Two Years of Waiting — And Now This: What Strip Center Owners Need to Know

For most of 2023 and 2024, strip center owners who considered selling faced a straightforward problem: the math didn't work. The Federal Reserve had pushed rates to multi-decade highs in its battle against post-pandemic inflation. Cap rate expectations expanded. The bid-ask gap widened. Buyers couldn't underwrite at prices sellers had anchored to. So owners held.

And for most of those two years, holding was the right call — not just financially, but operationally. Necessity-based and service-oriented tenants continued to perform. Occupancy held across most well-located centers. Rent collections stayed solid. The asset class kept generating income while the transaction market froze around it.

Then, heading into 2026, something shifted. The Fed began cutting. Buyer sentiment improved. Institutional capital, REITs, and private investors all started signaling renewed interest in strip centers — one of the few retail formats that had demonstrated genuine resilience through the rate cycle. The wait, it seemed, was paying off.

This week, however, delivered a more complicated message. Three significant developments arrived simultaneously, and strip center owners need to understand all three.

The Consumer Is Still Spending — But the Psychology Has Changed

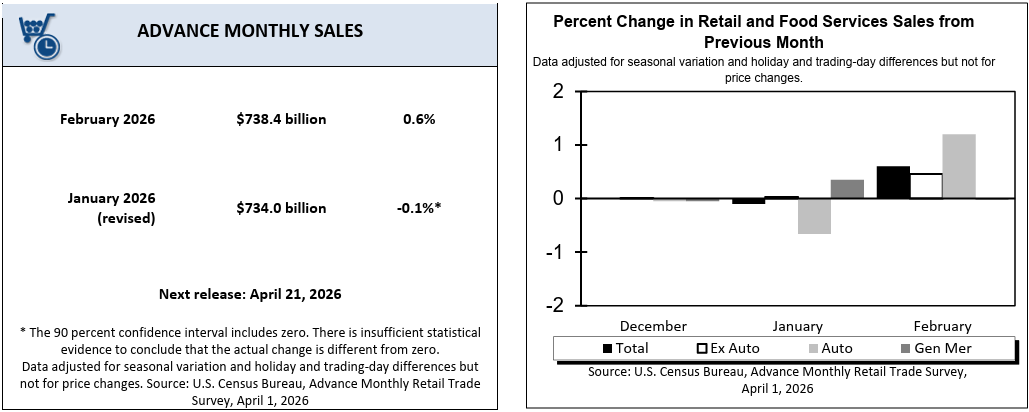

On April 1st, the U.S. Census Bureau released its advance monthly retail trade estimate for February 2026. Total retail and food services sales came in at $738.4 billion — up 0.6% from January and 3.7% above the prior year. By most measures, that's a healthy reading.

But layered beneath that headline is a consumer whose confidence in the future is eroding. The Conference Board's March 2026 Consumer Confidence report showed the Expectations Index — which measures forward-looking sentiment on income, business conditions, and the labor market — falling to 70.9. Historically, readings below 80 have often preceded economic deceleration.

In a single month, the share of consumers expecting higher interest rates over the next year jumped from 34.9% to 42.4%. Expectations for higher stock prices fell sharply. Vacation plans declined. The Conference Board pointed directly to oil price pressures and the ongoing conflict in Iran as the primary drivers.

What does this mean at the retail level? Service-based tenants with recurring, necessity-driven demand — medical, dental, beauty, fitness, pet services, quick service food, tax prep — remain the most durable performers in a cautious consumer environment. Fitness and beauty held relatively better than travel and big-ticket entertainment in this month's data.

The USDA Economic Research Service's food price data added further texture. Food-away-from-home prices rose 3.9% year-over-year through February 2026, outpacing food-at-home inflation of 2.4%. That spread creates behavioral pressure on dining decisions. Value-oriented quick service tends to hold. Mid-tier casual dining without a compelling value proposition faces a more challenging environment.

The Tariff Equation: Understanding the Law Behind the Numbers

On April 2nd, the Yale Budget Lab released its most comprehensive tariff analysis to date. The combined impact of all tariffs currently in place represents an average effective tariff rate increase of nearly 20 percentage points — with an estimated consumer price impact of approximately 2.3%, equivalent to roughly $3,800 in lost purchasing power per household.

To understand why this situation remains unsettled, it helps to know the legal mechanics — because the law governing these tariffs has changed twice in recent months and could change again.

The administration originally imposed sweeping tariffs on nearly every U.S. trading partner using a law called IEEPA — the International Emergency Economic Powers Act, passed by Congress in 1977. IEEPA gives the president broad authority to regulate international commerce when a national emergency has been declared. The administration argued that chronic trade deficits constituted such an emergency. In February 2026, the Supreme Court ruled 6 to 3 that IEEPA does not authorize tariffs. Those tariffs were struck down.

In response, the administration pivoted to Section 122 of the Trade Act of 1974. Unlike IEEPA, Section 122 does specifically authorize the president to impose emergency import tariffs — but it comes with two hard statutory limits: the rate cannot exceed 15%, and the authority expires after 150 days. Those Section 122 tariffs took effect February 24th. That 150-day clock is running.

What this means practically: if the administration wants to sustain tariffs beyond that window, it will need either a new legal mechanism or an act of Congress. Neither path is fast or certain. That uncertainty has a real economic cost that goes beyond the tariff rates themselves — businesses cannot confidently plan supply chains or pricing around a policy regime that may not exist five months from now. That hesitation filters through to investment decisions, hiring, and ultimately to consumer prices and tenant behavior.

For strip center owners, the relevant exposure varies by tenant type. Service-based tenants have relatively low import content in their cost structures. A nail salon, a fitness studio, a dental office, or a tax preparer is not materially affected by tariff-driven goods inflation. Goods-based tenants — particularly those selling electronics, apparel, home furnishings, or discretionary items with high import content — face more direct exposure.

There is one additional dynamic worth monitoring. The Yale Budget Lab analysis noted that firm-level import stockpiles built up ahead of the original 2025 tariff wave are now nearly depleted. Another wave of cost pass-through to retail shelves may occur in the coming months — even as the legal framework continues to evolve.

The Oil Shock: Iran, the Strait of Hormuz, and What April Brings

The third development this week is moving faster than either of the others, and it threads directly through the consumer picture and the rate environment: the oil shock from the conflict in Iran.

Here is the context. The United States and Israel launched military operations against Iran in late February 2026. Iran retaliated by effectively closing the Strait of Hormuz — a narrow waterway between Iran and Oman that serves as the chokepoint for roughly 20 percent of the world's daily oil supply, approximately 20 million barrels per day. Saudi Arabia and the UAE have rerouted some oil through alternative pipelines, but those routes have capacity limits and cannot offset a full strait closure. The U.S. and other governments have coordinated a record release from strategic petroleum reserves, providing some breathing room — but not a solution.

Brent crude oil surpassed $100 per barrel for the first time in four years in early March and has remained elevated and volatile. West Texas Intermediate, the U.S. benchmark, was trading above $112 per barrel as of Thursday. The International Energy Agency has characterized this as the largest supply disruption in the history of the global oil market — exceeding in volume both the 1973 Arab oil embargo and the 1979 Iranian Revolution.

The forward-looking picture is the part that matters most for the weeks directly ahead. The IEA's executive director stated this week that April will be significantly worse than March. The reason is straightforward: in March, cargo ships that had loaded in the Gulf before the conflict broke out were still making their deliveries to ports around the world. That pre-war pipeline is now cleared. In April, there is no new supply flowing through the strait.

Goldman Sachs has raised its probability of recession over the next 12 months to 30 percent. Gasoline prices in California have already exceeded $5 per gallon. Oil industry executives and analysts quoted this week said the strait needs to reopen by mid-April or supply constraints will escalate sharply — doubling the estimated supply loss from roughly 4.5 to 5 million barrels per day to upward of 10 million.

For strip center owners, the connection runs in two directions. First, higher energy costs compress household budgets. The consumer who is already absorbing tariff-driven price increases at the retail level is simultaneously paying more to fill a gas tank and heat a home. That household has less left to spend everywhere else — including at your tenants' stores. Second, sustained high oil prices feed inflation expectations, which feed Treasury yields, which feed the cost of capital on any acquisition or refinance your buyers or lenders are underwriting.

The Rate Environment: Why the Math Still Governs the Market

Strip center capital markets are meaningfully better than they were 18 months ago. Buyer appetite has improved. The recognition of neighborhood and unanchored strip centers as a resilient, necessity-driven asset class has expanded. Deal flow is increasing.

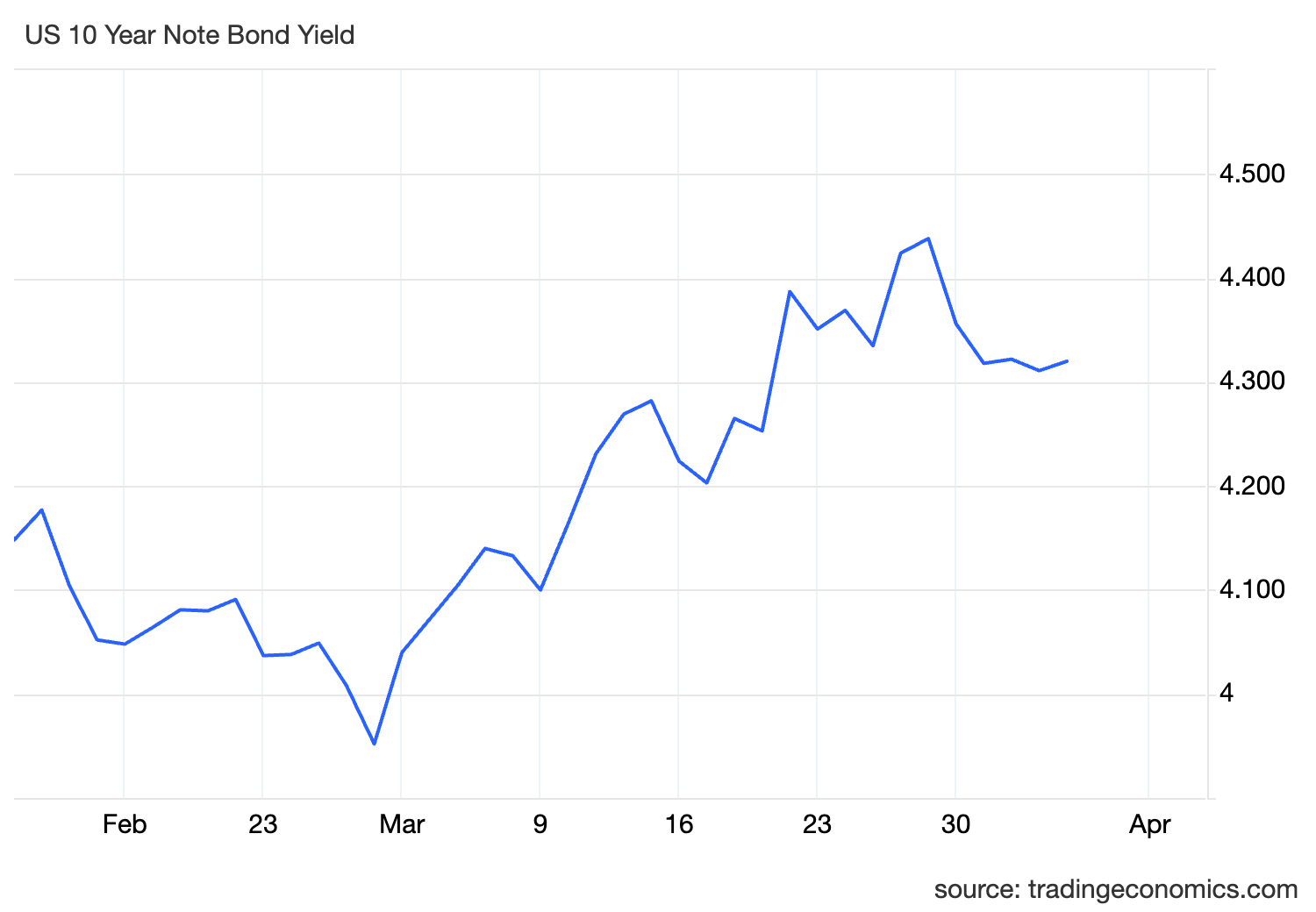

But the math on new acquisitions is still largely governed by one number: the 10-year Treasury yield.

The Federal Reserve's H.15 release shows the 10-year Treasury closing April 2nd at 4.31%, with intraday volatility driven by the Iran conflict and its implications for oil prices and inflation. Fed Chair Powell reaffirmed a wait-and-see posture this week, and markets have adjusted expectations accordingly — currently pricing in no Fed rate cuts for the remainder of 2026.

For strip center acquisition underwriting, lenders typically price their base rate off the 10-year and add a spread of 175 to 250 basis points depending on asset quality, market, sponsor, and loan structure. At today's 10-year, that produces effective loan rates in the 6.00% to 6.75% range. At those rates, lenders require debt coverage ratios that constrain what buyers can pay — particularly for assets that haven't had rent growth reset to market rates in the past 12 to 18 months.

The Iran conflict introduced a meaningful new variable this week. If elevated oil prices sustain and inflation expectations continue to rise, the 10-year could drift back toward the 4.5% to 4.75% range. That's not a certainty — but it is now a plausible scenario in a way it was not 30 days ago, and it is worth factoring into any near-term decision-making.

What This Means for Your Property

The two years of waiting were not wasted. They produced an asset class that has proven its durability, a tenant mix that has been stress-tested, and an owner base that has held through a difficult cycle with operational integrity intact.

The window that has opened in 2026 is real. But the conditions inside it are more complex than a simple "the market came back" narrative.

The owners who will navigate this environment most effectively are those operating from a clear-eyed, property-specific understanding:

Occupancy and lease term: A stabilized asset with strong tenancy and staggered lease expirations looks very different to a lender and buyer than one with near-term rollover risk — even if both properties appear similar on the surface.

Tenant mix quality: Service-oriented, necessity-driven tenants with strong unit economics are the most defensible position in the current consumer environment. Gaps in the lineup are worth addressing now, not after the next lease expiration creates urgency.

Rent-to-market: Properties where rents are below market provide a story for buyers that offsets rate pressure in underwriting. Properties where rents are at or above market need strong occupancy and credit quality to justify current pricing expectations.

Timing: The rate environment is fluid. The Iran conflict introduced new uncertainty this week that wasn't there 30 days ago. Owners who are close to a decision point — whether disposition, refinance, or re-leasing — benefit from making that decision with current data, not data from six months ago.

Final Thought

Strip center ownership has always rewarded patience. The two-year wait that most owners have endured reflects exactly that discipline.

What this week's data asks is not whether to act — it asks whether owners are making decisions with an accurate picture of where things actually stand. Consumer spending is real but cautious. Tariff law is unsettled in ways that matter for prices. An oil shock is actively compressing household budgets and threatening to push rates higher. And buyer appetite, while genuine, is still governed by math that requires clear-eyed underwriting.

If you want to talk through what this environment means specifically for your property — in San Antonio, Austin, or the Rio Grande Valley — I'm happy to have that conversation.

Watch or Listen on Youtube

Ray Kang, CCIM is an investment sales advisor specializing in retail strip centers across San Antonio, Austin, and the Rio Grande Valley, Texas. He operates under StripCenterIQ (stripcenteriq.com) and raycrebroker.com.

Sources:

U.S. Census Bureau, Advance Monthly Retail Trade Survey, April 1, 2026: https://www.census.gov/retail/marts/www/marts_current.pdf

The Conference Board Consumer Confidence Index, April 1, 2026: https://www.conference-board.org/topics/consumer-confidence/

USDA Economic Research Service, Food Price Outlook — February 2026: https://www.ers.usda.gov/data-products/food-price-outlook/summary-findings

Yale Budget Lab, State of U.S. Tariffs — April 2, 2026: https://budgetlab.yale.edu/research/state-us-tariffs-april-2-2026

Federal Reserve H.15 Selected Interest Rates, April 3, 2026: https://www.federalreserve.gov/releases/h15/

TradingEconomics, U.S. 10-Year Treasury Yield: https://tradingeconomics.com/united-states/government-bond-yield

IEA via CNBC, Oil Supply Disruption — April 1, 2026: https://www.cnbc.com/2026/04/01/oil-price-iea-fatih-birol-brent-iran-strait-hormuz.html

YourNews, Iran Conflict Supply Chain Impact — April 4, 2026: https://yournews.com/2026/04/04/6757332/iran-conflict-disrupts-global-supply-chains-driving-up-costs-for/