The Rate That Refuses to Fall: What This Week's Economic Data Means for Retail Strip Center Owners

Four weeks ago, the expectation across capital markets was straightforward: the Federal Reserve would cut rates twice in 2026, the 10-year Treasury would drift toward 3.5%, and the cost of capital for commercial real estate would ease. That was the tailwind retail property owners were counting on.

That tailwind is gone.

This week brought three converging data points — each significant on its own, more significant together — that retail strip center owners in San Antonio, Austin, and the Rio Grande Valley need to understand before making any decisions about their properties.

Consumer Sentiment: The Sharpest Post-Conflict Drop in the Data

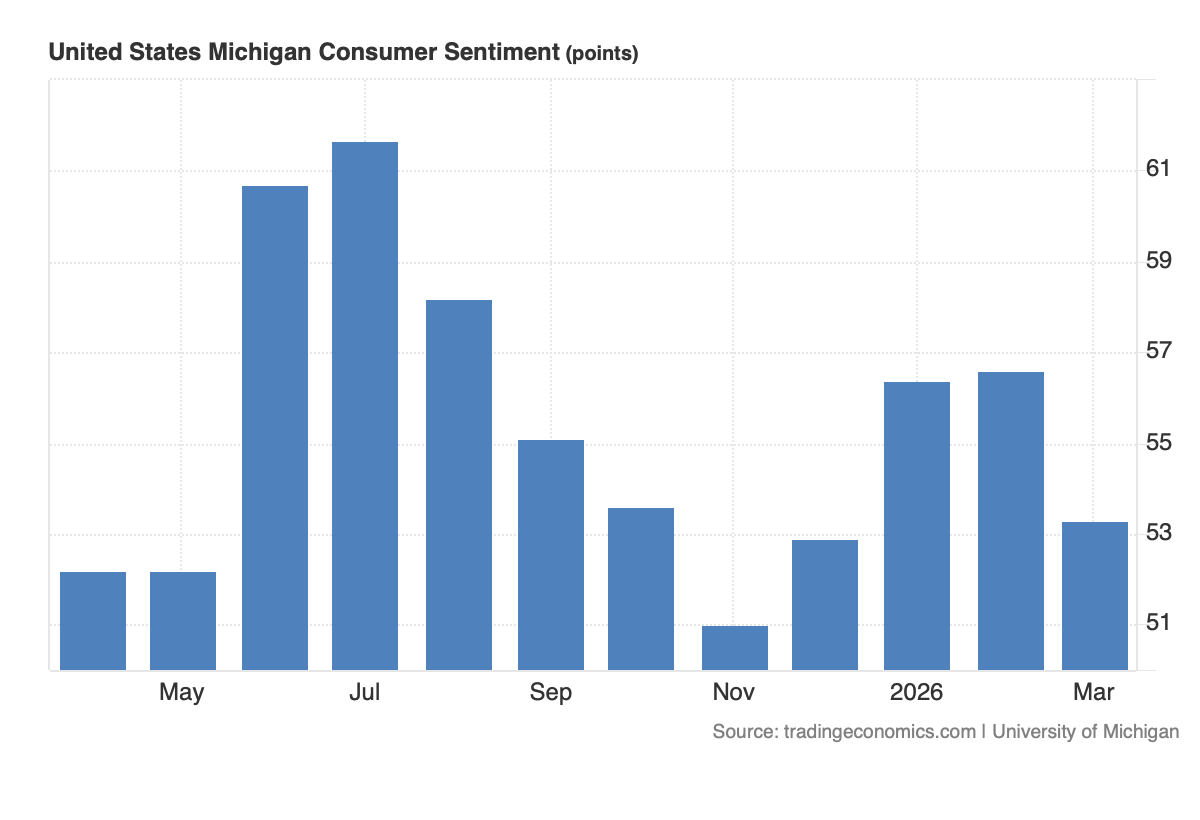

The University of Michigan released its final March 2026 Consumer Sentiment reading this morning. It came in at 53.3 — down from 56.6 in February and the lowest level since December. The reading landed in the bottom second percentile of the survey's entire history, dating back to 1978.

What makes this reading distinct from a typical monthly softening is the timing and the breadth. Surveys collected before February 28th were actually showing improvement. Once the U.S.-Israel military conflict with Iran began on that date, sentiment reversed sharply. The survey's director noted that the post-conflict interviews "completely erased" the gains from earlier in the month.

Two things in this report matter most for retail landlords. First, the decline was broad — not limited to lower-income consumers. Middle and higher-income households, including those with stock wealth, showed some of the steepest drops, buffeted simultaneously by rising gas prices and equity market volatility. Second, year-ahead inflation expectations jumped to 3.8% — the biggest monthly increase in approximately a year — signaling that consumers believe current pressures will persist, not fade quickly.

Source: University of Michigan Surveys of Consumers — Final March 2026 — released March 27, 2026

Gas at $3.98: When the Tax Refund Tailwind Becomes a Headwind

According to AAA, the national average price for a gallon of regular gasoline is $3.98 as of this week — up approximately 33% from one month ago. Diesel, which powers the delivery infrastructure behind virtually every retail supply chain, is up over 36%.

The mechanism is the effective closure of the Strait of Hormuz, the waterway through which roughly one-fifth of the world's oil supply moves. As long as that disruption persists, energy prices face structural upward pressure.

The energy price shock matters to retail property owners through two channels. The first is direct consumer spending reallocation. The NRF's chief economist framed it concisely: U.S. households spend approximately $2,500 a year, or roughly $50 a week, on gasoline. When that figure rises by $10 to $15 per week, that money comes out of somewhere. And the discretionary categories that get cut first are restaurants, entertainment, and non-essential retail — precisely the categories that anchor the tenant mix in most neighborhood and community strip centers.

The second channel is the erosion of the fiscal stimulus that was supposed to buoy consumer spending in early 2026. Larger-than-usual tax refunds tied to the Working Families Tax Cut Act were projected to provide a meaningful lift to retail sales in the first half of the year. Oxford Economics estimated that at a $3.60 average gasoline price, those refund gains would be almost exactly offset. The national average has passed that threshold. The refund tailwind is effectively gone.

Source: AAA Gas Price Data / CNBC citing Oxford Economics and National Retail Federation Chief Economist — March 26–27, 2026

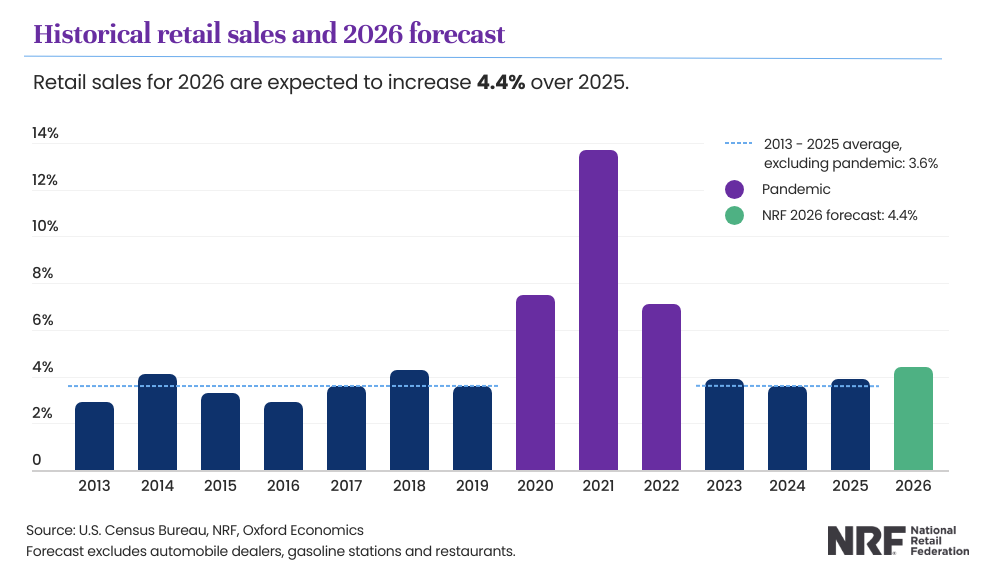

The NRF Forecast: 4.4% Growth With an Asterisk

Against this backdrop, the National Retail Federation issued its 2026 retail sales forecast last week: 4.4% growth over 2025, to a total of $5.6 trillion. Developed in partnership with Oxford Economics, it represents the highest projected growth rate since 2022 and exceeds the 10-year pre-pandemic average of 3.6%.

The NRF's case rests on durable fundamentals: real wage growth, solid household balance sheets, and an unemployment rate projected to remain below 4.5% for the year. These are not trivial inputs. The American consumer has consistently surprised to the upside even in difficult environments, and there is genuine underlying strength in the economy.

But the NRF was also explicit: the repercussions of the Iran conflict were too uncertain to incorporate into their forecast. The 4.4% projection is pre-conflict math. The NRF noted it would revise the forecast downward if the war's impact on retail sales became measurable.

The structural bifurcation in the forecast is also worth noting. Higher-income households are projected to drive the majority of retail spending growth in 2026. Lower-income households face compounding pressures from elevated gas prices, persistent food inflation, and limited balance sheet cushion. Which side of that divide your tenant mix serves has direct implications for income durability.

Source: National Retail Federation 2026 Retail Sales Forecast with Oxford Economics — March 18, 2026

Value Retail: The One Sector Positioned for This Environment

While much of the retail landscape is navigating headwinds, value-oriented retail continues to demonstrate remarkable resilience — and is expanding its customer base in ways that have real implications for strip center leasing strategy.

Grocery Dive reported this week that dollar store operators have been consistently noting gains with higher-income shoppers for several consecutive quarters. This is not a transient phenomenon — it reflects a structural shift in how consumers across income brackets think about value. Dollar Tree's management specifically cited the current gas price environment as a factor likely to accelerate that cross-income traffic shift. As they put it, their format is "that key tool that helps [consumers] manage their budgets."

Coresight Research's store opening tracker confirms the direction: Dollar General, Aldi, and Tractor Supply lead all retailers in planned new store openings for 2026. Value-oriented, convenience-focused, and essential-service retail is where expansion capital is flowing. Mall-dependent legacy formats, by contrast, continue to contract — with Macy's, GameStop, Walgreens, and others actively reducing their store counts.

For strip center owners, the implication is clear. Tenant lineups anchored by essential services, value retail, and food-and-beverage concepts that have demonstrated resilience through this consumer cycle are better positioned for income durability than those with heavy exposure to mid-tier discretionary categories.

Source: Grocery Dive — Wealthy Shoppers Heading to Dollar Stores — March 23, 2026

The Rate That Refuses to Fall — And What It Means for Your Property Value

Now to the data point that ties everything together for commercial real estate investors.

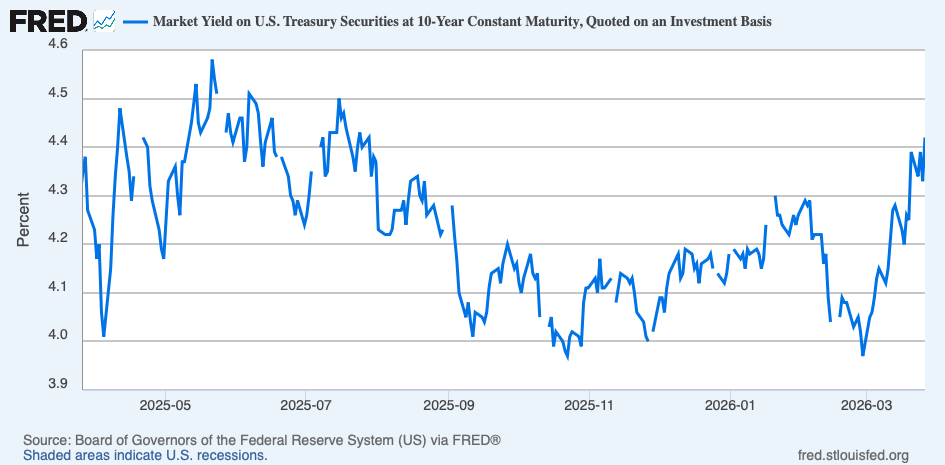

The 10-year Treasury note closed today at 4.44% — its highest level since July 2025. Earlier in the session it touched 4.48%. Four weeks ago, interest rate futures were pricing in two Federal Reserve rate cuts for 2026. Today, those same futures markets are pricing in nearly a 50% probability of a rate hike by December. That is not a modest adjustment in expectations. It is a complete reversal of the rate outlook in approximately 30 days.

The driver is the same chain of events we've described: conflict disrupts oil supply, oil prices rise, inflation expectations rise, Fed flexibility to cut evaporates, and the long end of the yield curve moves accordingly.

Understanding the borrowing rate connection

The 10-year Treasury matters to strip center owners primarily because commercial real estate lenders price loans off it. It's the base rate. Lenders then add a spread — typically 150 to 250 basis points above the 10-year, depending on the lender, the loan structure, and the deal profile. With the 10-year at 4.44% today, buyers in our markets are working with loan rates in roughly the 6% to 7% range. That is the real cost of capital on a strip center acquisition right now.

The practical consequence is straightforward. A buyer underwriting your property is running debt service coverage ratios and cash-on-cash return projections. When their loan rate moves from 6% to 7%, the deal math changes materially — either the acquisition price has to come down to make the numbers work, or the deal doesn't transact. That is the direct mechanism by which a rising 10-year becomes price pressure on your property. It isn't abstract — it is what happens at the negotiating table when a buyer's lender quotes a rate and the buyer runs the numbers.

Four weeks ago, buyers were underwriting with a rate assumption built on two expected Fed cuts in 2026. That assumption has been replaced by a market now pricing a nearly 50% probability of a rate hike by December. Deals that worked at one cost of capital don't work at another. That repricing doesn't happen overnight — buyers and sellers take time to adjust — but it accumulates. And it surfaces in the bids you receive when you take a property to market.

The implication is direct. When the 10-year rate rises instead of falling — when the rate refuses to fall — it exerts upward pressure on cap rates, which translates to downward pressure on property values, all else being equal.

The critical offsetting factor is net operating income growth. Properties where rents are growing, occupancy is strong, and leases are renewing at or above market can generate income growth that partially or fully counteracts cap rate expansion pressure on value. This is precisely why tenant quality, lease structure, and renewal execution matter so acutely in the current environment — they are not just operational concerns, they are value-preservation levers.

The U.S. Dollar Index (DXY) closed the week near 100 — up approximately 5% from its February low of 96. This safe-haven strengthening in the dollar reflects the same market dynamic: investors pricing elevated geopolitical uncertainty and a Federal Reserve constrained from the easing cycle that was expected just a month ago.

Source: Federal Reserve H.15 Selected Interest Rates / Advisor Perspectives Treasury Yield Snapshot — March 27, 2026Source: Trading Economics / Reuters — U.S. Dollar Index — March 27, 2026

What This Means Practically for Strip Center Owners

Three areas of focus are worth prioritizing in this environment.

Tenant mix review. The bifurcated consumer environment — value-oriented and essential-service tenants thriving, mid-tier discretionary tenants under pressure — is not a temporary condition. It reflects structural spending shifts that are being accelerated by the current energy price shock. Understanding where each tenant in your lineup sits on that spectrum, and which leases carry renewal risk in a softer consumer environment, is foundational work.

Lease renewal and NOI strategy. In an environment where the 10-year is holding elevated and cap rate compression is not available as a value tailwind, income growth becomes the primary driver of property value stability. Renewals executed at market rates, lease-up of any vacant space, and proactive tenant engagement ahead of expiration dates are the levers that matter most right now.

Disposition timing analysis. For owners who have been considering a sale — whether in the near term or within the next few years — the rate environment described in this week's data is a meaningful input to that analysis. The window where a declining 10-year was expected to compress cap rates and provide a natural value tailwind is not open today. That doesn't mean it is permanently closed — geopolitical situations resolve, rate cycles turn — but it does mean timing assumptions built on that tailwind need to be revisited against the current picture.

Summary

Consumer sentiment hit its lowest level since December. Gas is near $4 and rising, wiping out the tax refund tailwind that was expected to support retail spending. The NRF still projects 4.4% retail growth — but with the Iran conflict explicitly excluded from their model. Value retail is attracting shoppers across income brackets and leading all sectors in new store openings. And the 10-year Treasury, which was supposed to be declining toward 3.5% by now, closed today at 4.44% — its highest level since last July — with markets now pricing the possibility of a rate hike rather than cuts.

The rate that was supposed to fall is refusing to. For retail strip center owners, the response to that reality lives in tenant quality, lease execution, and clear-eyed timing analysis.

WATCH OR LISTEN ON YOUTUBE ▶️