Rate Relief Is Fading. Service Tenant Demand Isn't.

Retail Weekend Wrap-Up | Week of March 15–21, 2026 By Ray Kang, CCIM

WATCH OR LISTEN ON YOUTUBE ▶️

Two stories converged this week that, taken together, tell retail property owners something fundamental about where their centers are heading — and what to do about it. One is a headwind. One is an opportunity. The investors who hold both ideas at the same time are making better decisions than the ones focused on just one.

The Fed Held Rates. The Market Sold Off Anyway.

Source: Board of Governors of the Federal Reserve System (US) via ALFRED®

On Wednesday, March 18th, the Federal Reserve voted tohold the federal funds rate unchanged at a target range of 3.5% to 3.75% — the second consecutive meeting with no adjustment. The decision matched market expectations nearly perfectly.

The Dow closed down 770 points. The S&P 500 fell 1.36%. The Nasdaq declined 1.46%.

When markets sell off on exactly the news they anticipated, the signal is worth reading carefully. The anxiety is not about what the Fed did — it's about what the Fed cannot do.

The Dot Plot Shifted Toward Fewer Cuts

The Fed's Summary of Economic Projections — commonly called the dot plot — still reflects a median projection of one rate cut in 2026, unchanged from December. But the composition underneath that median is moving. Seven of the nineteen FOMC members now expect zero cuts this year, up from six in December. One more voice saying rates should stay where they are. The hawks are gaining.

The committee also revised its projections upward in two key areas: GDP growth for 2026 was raised to 2.4%, and core PCE inflation — the Fed's preferred measure — was raised to 2.7% for the year. An economy growing faster than expected while inflation is being revised higher is exactly the environment in which the Fed cannot justify cutting rates, regardless of what the market wants.

The Energy Shock Is Already in Your Tenants' Customers' Wallets

To understand why the Fed is stuck, you have to understand what happened on February 28th.

The United States and Israel launched joint airstrikes on Iran. Within days, the Strait of Hormuz — through which approximately 20 million barrels per day of crude and petroleum products flow — was severely disrupted. Brent crude oil spiked toward $120 per barrel at the peak, before partially retreating. As of theU.S. Energy Information Administration's March 10th Short-Term Energy Outlook, Brent was trading around $94 per barrel — up approximately 50% since the start of the year.

The EIA projects crude prices will remain above $95 per barrel for the next two months before easing later in 2026. That is not a temporary blip.

The consumer consequences are already playing out.According to PBS NewsHour's reporting, Moody's chief economist Mark Zandi estimated gasoline could approach $4 per gallon in the near term. Gregory Daco at EY-Parthenon estimated the energy shock could push March monthly inflation to near 1% — the highest single-month reading in four years. JPMorgan analysts project annual inflation could reach 3% or higher.

TheNational Retail Federation's chief economist noted that the average American household spends roughly $2,500 annually at the gas pump — about $50 per week. For lower-income shoppers, a sudden surge per gallon is a budget event that is felt immediately, not months from now.

This is not abstract. This is the customer pulling into your center's parking lot — deciding before they walk in how much they have to spend.

What This Means for the Rate Environment and Your Property

The 10-year Treasury yield climbed back above 4.2% this week as energy-driven inflation expectations pushed bond investors to demand higher returns. PerBankrate's March 19th mortgage rate report, the 30-year fixed mortgage rate rose to approximately 6.29–6.33% — up from around 6.09% just one month earlier.

Fixed mortgage rates track the 10-year Treasury, not the federal funds rate. When inflation expectations rise, Treasury yields rise, and mortgage rates follow. The same dynamic that makes homebuying more expensive also applies to commercial real estate financing.

The FOMC's next meeting is April 28–29. Analysts at J.P. Morgan have already stated they do not expect any cuts in 2026 at all. The Mortgage Bankers Association projects the 30-year rate remaining in a 6.0–6.5% range through year-end. The easing cycle that retail property owners were counting on to compress cap rates and lower refinancing costs has been pushed further out — again.

For retail property owners: If you carry a loan maturing or a refinance event in the next 12 to 18 months, this week was not good news. The window for rate relief is narrowing, and the bar for cuts is rising. This is not a moment to panic — but it is a moment to plan deliberately around your capital stack.

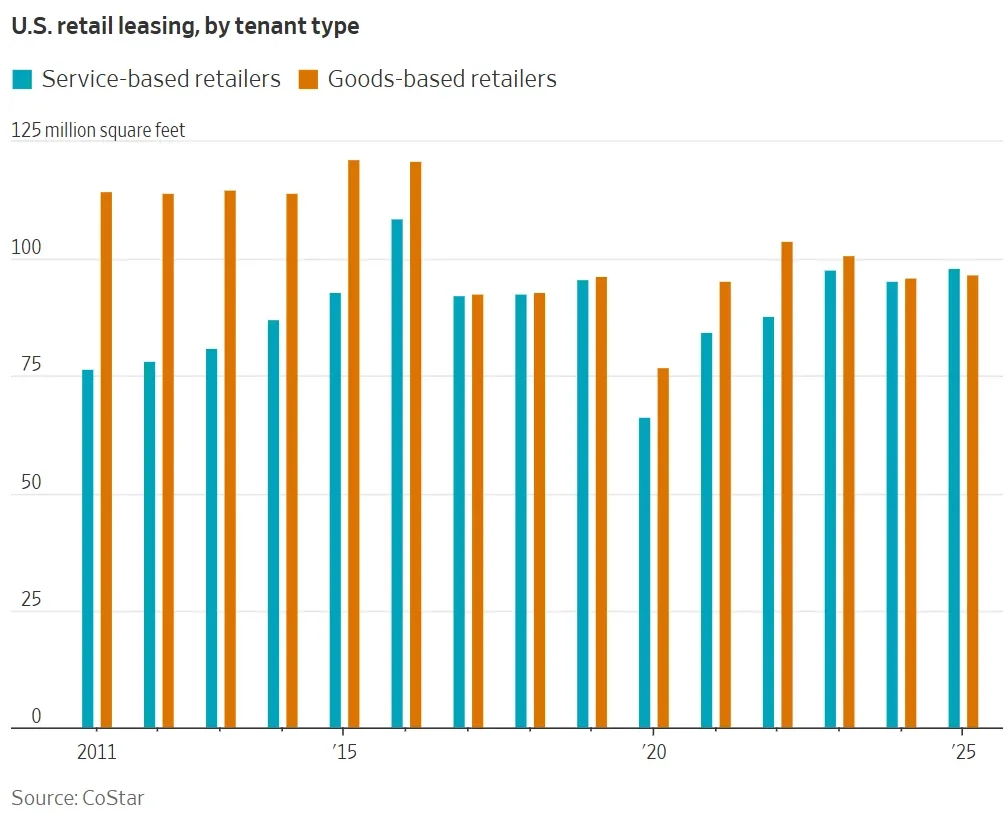

For the First Time in History, Services Beat Goods in Retail Leasing

Now here is the story that changes how you think about your strip center.

The Wall Street Journal reported this week, citing data from CoStar Group, that in 2025 — for the first time in recorded retail real estate history — service-based tenants leased more total retail square footage in the United States than goods-based retailers.The Real Deal covered the findings on March 18th.

The split was narrow: 50.4% services, 49.6% goods. But narrow or not, the crossover is historic.

Brandon Svec, CoStar's national director of U.S. retail analytics, told the Journal: "Consumer dollars remain firmly pointed at services. There's nothing to suggest that's going to be shifting anytime soon."

Fifteen years ago, service tenants represented only 40% of retail leasing. In a decade and a half, their share rose ten percentage points — steadily, consistently, and now past the majority line for the first time ever.

What Is a "Service Tenant"?

When CoStar and the Journal refer to service tenants, they mean businesses that deliver an experience in person that fundamentally cannot be replicated online: gyms, fitness studios, boutique fitness concepts, spas, nail salons, hair salons, med spas, cryotherapy, IV drip bars, pickleball facilities, personal training studios, urgent care clinics, dental offices, optometry practices, veterinary services, tax preparation offices, insurance offices, and more.

These businesses share a critical characteristic: they require the customer to physically show up. You cannot get a blowout delivered. You cannot do a HIIT class through a shopping cart. You cannot get a dental exam fulfilled by a third-party logistics provider. They are, by definition, e-commerce-proof.

Fitness Was the Headline Growth Story

CoStar's underlying data highlighted fitness as one of the strongest service-sector leasing growth stories of 2025. Consumer prioritization of health and wellness drove meaningful expansion among both national operators and specialized local concepts. Fitness tenants have proven particularly effective at absorbing second-generation retail space — including former big-box and junior anchor locations — making them valuable partners for landlords managing large-format vacancies. They drive consistent foot traffic at high frequency, extending across morning, midday, and evening hours in ways that benefit neighboring tenants throughout the day.

Entertainment retail also grew its leasing share, extending a multi-year trend toward experiential concepts: immersive experiences, recreation facilities, social activity spaces. These, too, require a physical presence to function.

Vacancy Remains Near All-Time Lows — Because of This Shift

Perhaps the most striking finding is that despite the store closure headlines dominating retail coverage in early 2026,U.S. retail vacancy held at 4.4% — near record lows.

The reason is service tenants. Every time a goods-based retailer vacates a bay, a fitness studio, a spa, a medical tenant, or a personal care brand is waiting to absorb it. Service tenants are not filling a niche in the retail leasing market. They are sustaining it.

The Restaurant Exception Worth Noting

CoStar's data included one important nuance: restaurant leasing fell to its lowest post-pandemic level at just 16.8% of total service leasing — even as consumers spent more than ever on food away from home. Restaurant operators are becoming highly deliberate about which centers, which trade areas, and which co-tenancy configurations justify a lease commitment. For strip center owners, this means generic pitch decks won't move the needle with restaurant tenants. What moves the needle is specific, credible data about your trade area, co-tenancy, and traffic patterns.

What Strip Center Owners Should Do With This Information

These two stories are not contradictory. They are complementary. The macro environment is creating consumer pressure. The leasing environment for service-oriented space is absorbing it. Together, they define the playing field.

Four strategic implications:

1. Your vacant bay may have more demand than you realize. Service tenants are not searching for the lowest rent per square foot. They are searching for the right location, the right co-tenancy, and the right traffic pattern. If your center is in a submarket with favorable demographics for wellness, personal care, or healthcare-adjacent uses, you are likely sitting on demand you haven't fully tapped.

2. Your tenant mix is your competitive moat. A strip center anchored by a gym, supported by a nail salon, a med spa, an urgent care, and a dental office is a center that e-commerce cannot touch. Every one of those tenants requires the customer to appear in person, often repeatedly. That frequency of visit — that physical necessity — is the most durable thing you can own in retail real estate right now.

3. Don't reflexively renew a struggling goods-based tenant below market. If you have a clothing store, phone accessories shop, or similar goods-focused tenant whose performance has been declining, this data should inform your thinking about their upcoming renewal. The service tenant demand is real. Know your alternatives before you concede on price.

4. The repositioning window is open. A center that was 70% goods-based five years ago can be repositioned over time toward service tenants. It does not happen overnight, and it requires intentional leasing strategy. But the demand is there, and the consumer's spending behavior is pointing in one direction. The time to act is not when your center has 30% vacancy. It is now, one lease at a time.

Bringing It Together

The Federal Reserve held this week, and the rate environment got murkier, not clearer. Oil prices are elevated, inflation expectations are rising, the 10-year Treasury is climbing, and the path to rate cuts is narrowing. Lower-income consumers are being hit at the pump in real time, and that will show up in tenant performance at centers serving budget-constrained households.

At the same time, the physical retail market — particularly for service-oriented space — is as structurally healthy as it has been in a generation. For the first time ever, services lead retail leasing. Vacancy is near record lows. The tenant category that e-commerce cannot kill is actively expanding and absorbing space.

The investor who holds both of those realities clearly, and makes decisions from that full picture, is the investor best positioned for what comes next.

Sources:

FOMC Statement — March 18, 2026 | Board of Governors, Federal Reserve System

Short-Term Energy Outlook — March 10, 2026 | U.S. Energy Information Administration

Fed Holds Rates Steady — March 18, 2026 | Charles Schwab

The Iran War and Surging Oil Prices Are Affecting Consumers | PBS NewsHour

Mortgage Rates Today — March 19, 2026 | Bankrate

NRF Forecasts 4.4% Annual Retail Sales Growth — March 18, 2026 | National Retail Federation

Service-Oriented Leasing Surpasses Goods-Based Tenants — March 18, 2026 | The Real Deal / WSJ / CoStar

Service Tenants Dominate Retail Leasing Market — March 18, 2026 | CRE Daily / CoStar

Fitness Centers, Pickleball Courts, Other Services Now Dominate Retail Real Estate — March 9, 2026 | NNN Fitness / CoStar Insight