Same Week. Two Completely Different Economies. | Retail Weekend Wrap-Up

Retail Weekend Wrap-Up | Week of March 14, 2026

By Ray Kang, CCIM | Investment Sales · Retail Strip Centers | San Antonio · Austin · Rio Grande Valley

In the span of seven days, the U.S. economy produced two headlines that seem impossible to reconcile.

Jobs fell 92,000 in February — nearly double what economists expected. Consumer sentiment dropped to its lowest reading of 2026, sitting historically in the 2nd percentile of all readings since 1978. A major national department store chain reported its fourth consecutive year of sales declines and warned that its core customers are pulling back on discretionary spending.

And in the same week, Dollar General Corporation reported record annual revenues of $42.7 billion and announced plans to open 450 new stores.

Both of those things are simultaneously true. And that split — that bifurcation between where consumers are pulling back and where they are actively spending — is the most important thing a retail strip center owner can understand right now.

WATCH OR LISTEN ON YOUTUBE ▶️

The Economic Data Released This Week

BLS February Jobs Report: Worse Than Expected

The Bureau of Labor Statistics released the February Employment Situation on March 6th. The economy shed 92,000 jobs — the consensus estimate was -50,000. Unemployment rose to 4.4%, and February marked the third payroll decline in the past five months.

Average hourly earnings remain positive, up 3.8% year-over-year, which means employed workers are still seeing real wage growth. But long-term unemployment — those out of work for 27 weeks or more — reached its highest level since December 2021. That represents a different category of economic pressure: workers who have been displaced and are struggling to re-enter, not simply between jobs.

For retail property owners, a softening job market matters most through its effect on discretionary consumer spending. Tenants whose business models depend on customers feeling financially confident are the most exposed.

January Retail Sales: Read Past the Headline

The Census Bureau’s advance retail sales estimate for January, also released on March 6th, came in at -0.2% month-over-month — below expectations and weaker than December’s flat reading. Motor vehicle dealers and gasoline stations drove the decline.

The measure economists watch most closely for underlying spending trends told a different story. The “control group” — which excludes autos, gasoline, building materials, and food services — rose 0.3% in January, suggesting that core consumer activity was more resilient than the headline indicated. Year-over-year, total retail sales are still up 3.2%.

One additional factor worth monitoring: federal tax refunds are running approximately 20% above last year’s pace. Economists broadly expect this to provide a meaningful boost to consumer spending in March and April, which means the current data snapshot may be more temporary than it appears.

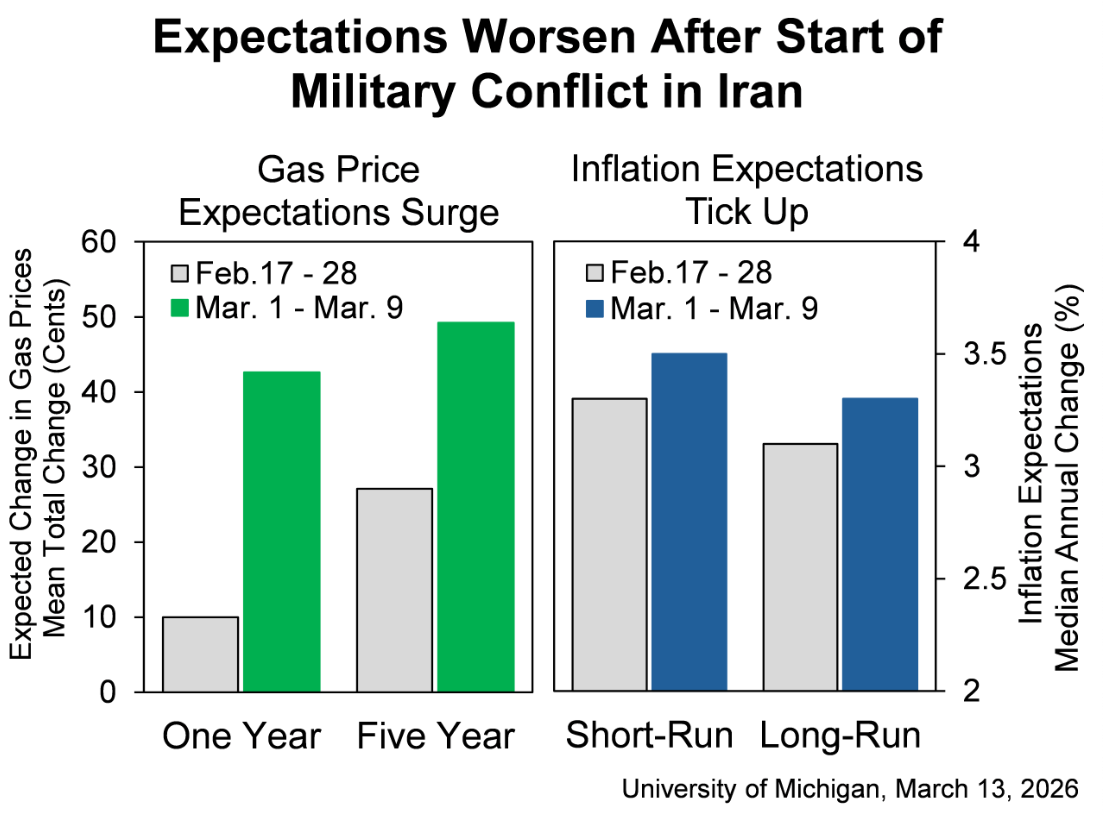

University of Michigan: Sentiment at Historic Low — Released Today

The University of Michigan’s preliminary March consumer sentiment reading came in this morning at 55.5, down from 56.6 in February. That is the lowest reading of 2026 to date — and in historical context, the index is currently sitting in the 2nd percentile of all readings in the survey’s history dating back to 1978.

The survey director, Joanne Hsu, noted a clear inflection point within the data itself. Interviews completed before the U.S. military action in Iran showed improvement from February. Interviews conducted in the nine days following the start of the conflict completely reversed those gains. Rising gasoline prices — up roughly 25 cents per gallon in just the first week of March — represented the most immediate and tangible consumer pressure.

One additional signal worth tracking: year-ahead inflation expectations stalled at 3.4% this month after six consecutive months of decline. That reversal, however modest, suggests the disinflationary trend may be temporarily pausing.

Source: Kohl’s

Kohl’s Q4 Earnings: Mid-Tier Discretionary Under Pressure

Kohl’s Corporation reported fourth-quarter and full-year fiscal 2025 results on March 10th. Net sales declined 3.9% in the quarter and 4.0% for the full year. Comparable sales fell 2.8% and 3.1% respectively.

The company’s CFO, Jill Timm, was direct on the earnings call: Kohl’s core customer base — low to middle-income households — is being “choiceful” with discretionary spending. The retailer issued 2026 guidance projecting comparable sales ranging from flat to a 2% decline.

That word — choiceful — deserves attention. It signals that the spending behavior shift underway is deliberate, not panic-driven. Consumers are making conscious trade-offs about where their dollars go. They are not necessarily spending less in aggregate; they are spending differently. And where those redirected dollars flow is the story of retail real estate in 2026.

What’s Happening at the Tenant Level

Dollar General: Record Revenue, 450 New Stores — Same Week

On March 12th, Dollar General Corporation reported fiscal year 2025 results: record net revenue of $42.7 billion, a 5.2% increase over the prior year. Q4 same-store sales rose 4.3%, with growth in both customer traffic and average basket size. For fiscal 2026, the company announced plans to open approximately 450 new stores, remodel approximately 4,250 existing locations, and invest between $1.4 and $1.5 billion in capital expenditures.

The same week that Kohl’s — a mid-tier department store serving low-to-middle income households — reported four consecutive years of sales declines, Dollar General — a value retailer serving many of the same households — reported record revenues.

Source: Dollar General

This is not coincidence. This is the bifurcation made visible in real earnings data. When consumers get “choiceful” about discretionary spending, some of those trade-off dollars flow to value-necessity retail. Dollar General’s growth strategy is built precisely around that dynamic: their expansion targets rural and small-town markets where 80% of their existing base is located, serving communities with limited retail options and price-sensitive households.

For retail strip center owners and investors, Dollar General represents active lease demand in the neighborhood and strip center format. Their expansion signals where consumers are spending and validates the location economics of the markets they enter.

The split between value retail and mid-tier discretionary is no longer a forward-looking trend. It is in reported quarterly earnings from this week. Kohl’s is down four straight years. Dollar General is at record revenue. Your tenant mix is positioned on one side of that divide or the other. Understanding which side is the foundational question for your asset strategy in 2026.

If you have a struggling full-service restaurant in your center, act now — not reactively.

Nine percent closure risk is a material figure. Review your leases, identify your co-tenancy exposure, and begin exploring replacement options before a vacancy materializes. The operators who engage proactively will protect their NOI. Those who wait for a missed rent check will spend the next 12 months playing catch-up.

Don’t make long-term decisions based solely on this week’s sentiment reading.

Consumer sentiment is at historically low levels, but the drivers include gas price shock and geopolitical anxiety — factors that can shift relatively quickly. Tax refunds running 20% above last year represent a genuine near-term spending tailwind. The spring data may tell a different story. Use this window to do your homework, understand your exposure, and position yourself to move decisively when the picture clarifies.

About Ray Kang, CCIM

Ray Kang, CCIM is a commercial real estate investment sales professional specializing in retail strip centers across San Antonio, Austin, and the Rio Grande Valley, Texas. His practice focuses on helping private property owners maximize returns through market intelligence, hold-period advisory, and disposition strategy. He and his team have closed over a quarter billion dollars in retail investment sales volume over the past five years.

For a confidential conversation about your property or market, reach out at raycrebroker.com.

Sources

U.S. Bureau of Labor Statistics, Employment Situation February 2026 — bls.gov | U.S. Census Bureau, Advance Monthly Retail Sales January 2026 — census.gov | University of Michigan Surveys of Consumers, Preliminary March 2026 — sca.isr.umich.edu | Kohl’s Corporation, Q4 and Full Year Fiscal 2025 Results — investors.kohls.com | Dollar General Corporation, Q4 and Full Year Fiscal 2025 Results via Business Wire — businesswire.com | Restaurant Dive / Black Box Intelligence, Full-Service Restaurant Closure Risk 2026 — restaurantdive.com