The Energy Tax: What This Week's CPI, Jobs, and Sentiment Data Mean for Strip Center Owners

Retail Weekend Wrap-Up | April 12, 2026

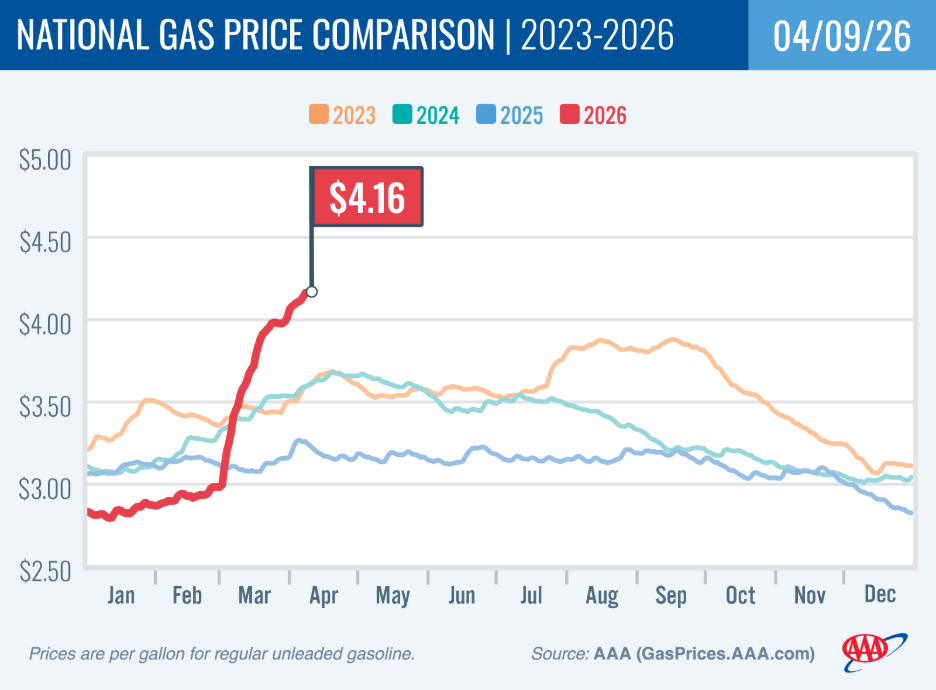

There's one number that connects every major data release this week: $1.08.

That is how much the national average price for a gallon of regular gasoline rose in a single month. The AAA national average reached $4.16 per gallon on April 9th — the highest level since August 2022 — driven by the energy shock from the U.S.-Iran conflict and the partial disruption of Strait of Hormuz oil traffic. According to AAA, that's $1.08 more than just one month ago.

That number doesn't just live at the pump. It flows directly into your CPI report, your consumer sentiment reading, your restaurant tenant's traffic count, and ultimately into the confidence level of every buyer and seller operating in commercial real estate today.

This week, we received four major data releases in rapid succession. Here's what each one means for strip center owners and investors.

CPI — March 2026: An Energy-Driven Spike With a Contained Core

The Bureau of Labor Statistics released the March 2026 Consumer Price Index on April 10th. Headline inflation rose 0.9% for the month, pushing the annual rate to 3.3% — the highest reading since April 2024 and up significantly from 2.4% in February. According to BLS, gasoline surged 21.2% in March alone and accounted for nearly three-quarters of the entire monthly price increase.

The nuance that matters for assessing the broader inflation picture: core CPI — excluding food and energy — rose just 0.2% for the month and 2.6% year-over-year, coming in a tenth of a point below forecast. Shelter inflation fell to 3.0% annually, tied for its lowest level since August 2021. Food prices were flat for the month. Medical care and household furnishings showed elevated year-over-year gains, but the broad-based, across-the-board inflation pressure of 2022–2023 is not what's driving this report. This is an energy shock with a contained underlying core — for now.

The figure most relevant to strip center owners is not the headline rate. It is this: real average hourly earnings fell 0.6% for the month. Wages increased 0.2%. Prices increased 0.9%. Your tenants' customers are falling behind. Their paychecks buy less in April than they did in February. That spending squeeze is the invisible pressure on your tenant base — and it will show up in traffic and ticket sizes before it shows up in lease stress.

Jobs — March 2026: A Strong Headline on a Slow Foundation

The March jobs report, released April 3rd, added 178,000 nonfarm payrolls — nearly three times the 59,000 consensus forecast. The unemployment rate edged down to 4.3%. On the surface, encouraging.

The deeper read is more cautious. February was revised down to a loss of 133,000 jobs. The three-month average payroll gain sits around 68,000 — a slow-growth labor market holding the line, not accelerating. The unemployment rate improvement came largely from 396,000 people leaving the labor force, not from a surge in employment. Labor force participation fell to 61.9% — near its lowest since 2021.

Healthcare and social assistance carried most of the weight in March, continuing a pattern of concentrated growth in a single sector. Long-term unemployment — those out of work 27 weeks or more — is up 322,000 over the past year. The JOLTS hiring rate has fallen to levels last seen in the depths of the COVID and GFC recessions.

For strip center investors, this labor market profile supports a cautious consumer spending environment. Customers still have jobs. But they're not feeling economic momentum — they're feeling stagnation, which in the context of an energy price shock, translates to defensive, value-oriented spending behavior.

Consumer Sentiment — April 2026: An All-Time Record Low

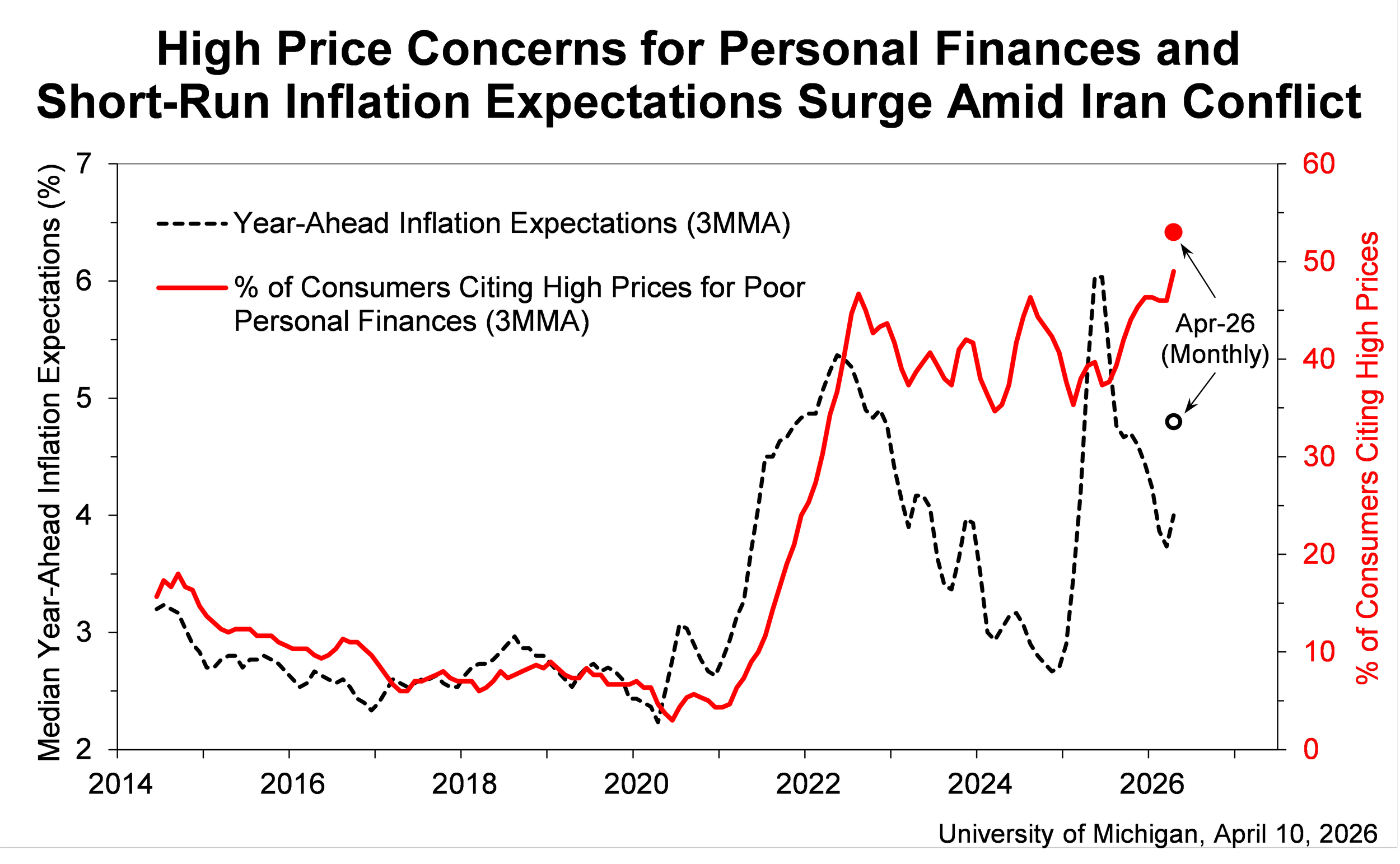

The most significant data point of the week arrived alongside the CPI this morning. The University of Michigan's preliminary Consumer Sentiment Index for April came in at 47.6 — a record low. That reading is below the prior all-time low of 51.7, set during the 1980 energy crisis. It is down 11% from March and 9% below a year ago.

Every demographic group posted setbacks simultaneously — every age bracket, every income level, every political affiliation. Every component of the index declined. One-year inflation expectations surged from 3.8% to 4.8% — the largest single-month increase since April 2025 and the highest level since 2024. Long-run inflation expectations rose to 3.4%, the highest since November 2025.

University of Michigan Survey Director Joanne Hsu noted that open-ended respondent comments show many consumers specifically blame the Iran conflict for unfavorable changes to the economy. One-year business condition expectations fell 20%. Personal finance assessments dropped 11%.

The critical caveat: 98% of these survey interviews were completed before the April 7th ceasefire announcement. The Michigan survey director acknowledged that economic expectations will likely improve once consumers gain confidence that the supply disruptions have ended and gas prices have moderated. That is the potential turning point. But "likely improve" is conditional. The ceasefire is fragile. Crude oil futures remain elevated near 2022 highs. And consumer sentiment — as we have seen over the past several years — can take far longer to recover than it does to fall.

We are watching this data, not celebrating a turning point that has not yet arrived.

The Rate Environment: No Relief in Sight

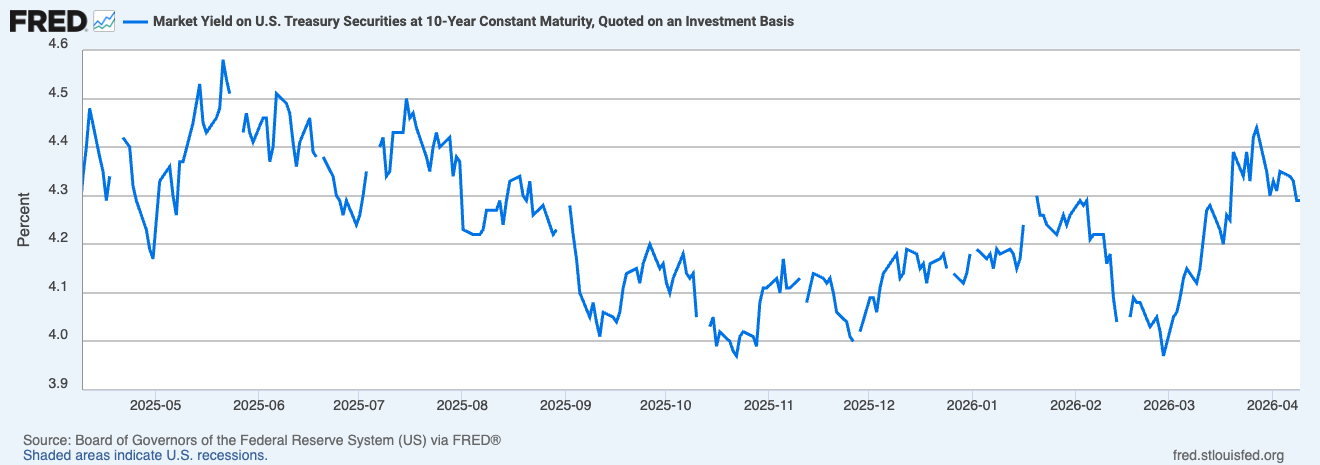

The 10-year Treasury closed April 10th at 4.31%, with the 2-year at 3.81% and the 30-year at 4.91%. Fed Chair Jerome Powell signaled a wait-and-see approach this week, acknowledging the energy-driven inflation spike but indicating the Fed needs to see the supply disruption confirmed as temporary before adjusting policy.

Markets are pricing virtually no probability of a rate cut at the April 28–29 FOMC meeting and a roughly 77% probability of no cuts through year-end. For strip center owners and investors, the practical translation is straightforward: commercial mortgage rates are starting in the mid-to-upper 5% range, using the 10-year Treasury as the base plus lender spreads of 150–250 basis points depending on property type, leverage, and sponsor profile. That math has not changed materially from recent months. The higher-for-longer environment remains the operative reality.

Financial decisions — refinancing, acquisition underwriting, sale timing — need to be evaluated against today's actual cost of capital, not against an expected rate environment that has not materialized.

The Restaurant Tenant Report: Bifurcation, Not Collapse

Restaurants represent one of the most common tenant categories in strip centers. And the restaurant industry is currently experiencing a bifurcation unlike anything seen outside of a recessionary environment — not uniform decline, but a dramatic divergence between concepts positioned for the current consumer environment and those that are not.

The traffic picture. Consumer confidence has declined 14 index points since 2023. Research from Revenue Management Solutions shows a 10-point confidence drop correlates with a 0.5–2% decline in restaurant traffic within two months. According to Black Box Intelligence, only about one-third of tracked restaurant brands posted positive comparable sales in 2025. Circana projects industry-wide traffic growth of less than 1% in 2026 — effectively flat.

The bifurcation. The spread in performance across concepts is extraordinary. In Q3 2025, Restaurant Dive tracked same-store sales across major public chains: Chili's posted 21.4% comparable sales growth. Sweetgreen fell 9.5%. A 31-point gap between the best and worst performer in the same quarter. The dividing line is clear — operators competing aggressively at the $10–$12 price point are taking share. Premium-priced concepts are losing it to them.

The standout growth category. Mexican and Latin limited-service restaurant concepts are the strongest-performing category in the current environment. Santiago & Company's transaction data shows purchase frequency at Mexican LSR chains increased more year-over-year than any other limited-service category. Cava continues to outperform. For strip center owners evaluating vacancies or lease renewals, this category is operating from a position of relative demand strength.

What consumers actually do when they cut back. McKinsey's restaurant research found that when consumers plan to reduce restaurant spending, most do not abandon their usual restaurants — they stay loyal but use more promotions, order fewer items, or trade down within the menu. The implication for your tenants: operators who quietly cut portion sizes or reduce ingredient quality to protect margins are risking the moment where a cost-conscious but loyal customer becomes a permanently lost one. The tenant question worth asking is not just whether rent is paid — it is whether the value proposition is holding.

The Investment Market: A Directional Signal Worth Noting

The Boulder Group released its Q1 2026 Net Lease Research Report this past week, containing a noteworthy data point: overall single-tenant net lease cap rates compressed for the first time in 15 consecutive quarters — one basis point, to 6.80%.

Boulder Group President Randy Blankstein noted that this compression occurred despite the 10-year Treasury reaching 4.48% late in the quarter and the Fed holding rates at both its January and March meetings. The compression reflects the depth and consistency of investor demand for net lease assets as a category. Supply of available net lease properties fell 9.8% quarter-over-quarter — more buyers competing for fewer available properties.

Retail net lease cap rates held at 6.55% for the second consecutive quarter. Bid-ask spreads narrowed two basis points to 23 basis points in Q1, reflecting sellers adjusting price expectations to align with where buyers are underwriting today.

Strip center cap rates run typically 100–150 basis points wider than single-tenant NNN, reflecting the multi-tenant structure and the operational characteristics of the asset class. But directional moves in the net lease investment market tend to lead what happens in multi-tenant retail pricing. The first compression in 15 quarters is not a dramatic shift. But the direction matters.

Practical Takeaways for Strip Center Owners

Know your tenant mix in this consumer environment. Service businesses — insurance, tax preparation, medical, personal care — and value-oriented food service are in a more defensible position than discretionary retail or full-price casual dining. If your center skews toward services and value, you may be better positioned than the macro headlines suggest.

Evaluate financial decisions at today's cost of capital. The 10-year is at 4.31%. Commercial mortgage rates are in the mid-5% range. The Fed is not cutting. Refinancing decisions, sale timing, and acquisition underwriting should be built on current rates — not on anticipated relief that is not visible in the near-term data.

Watch the investment market direction. The first cap rate compression in 15 quarters in the NNN market, combined with falling property supply, is a signal worth tracking. It does not change the immediate calculus for most strip center owners, but it suggests that investor demand for income-producing retail real estate remains durable even in a difficult macro environment.

Closing Thought

The ceasefire is a potential turning point. Consumers do not yet feel it — because they still see $4.16 at every gas station they pass. When that number comes down, and when they believe it's going to stay down, the sentiment data will follow. The question is how long that takes, and how fragile the ceasefire proves to be in the interim.

In the meantime: the data, not the headlines, is your guide.

WATCH OR LISTEN ON YOUTUBE ▶️

The full video version of this week's Wrap-Up is live on the StripCenterIQ YouTube channel.

Ray Kang, CCIM is a commercial real estate investment sales advisor specializing in retail strip centers across San Antonio, Austin, and the Rio Grande Valley, Texas. He advises strip center owners on hold strategy, timing, and disposition.

© 2026 raycrebroker.com — All rights reserved.