Strong Month, One Soft Line: What May's Retail Sales Mean for Strip Center Owners

The Retail Weekend Wrap-Up — June 13–19, 2026 By Ray Kang, CCIM

This was one of those weeks where the headline number and the useful number are two different things. The consumer looked strong. But there's a single line in the report that tells you which of your tenants is about to feel pressure — and it connects to oil, gas, and a negotiation that fell apart on Friday. Here's how I'm reading it for strip center owners.

A genuinely strong consumer

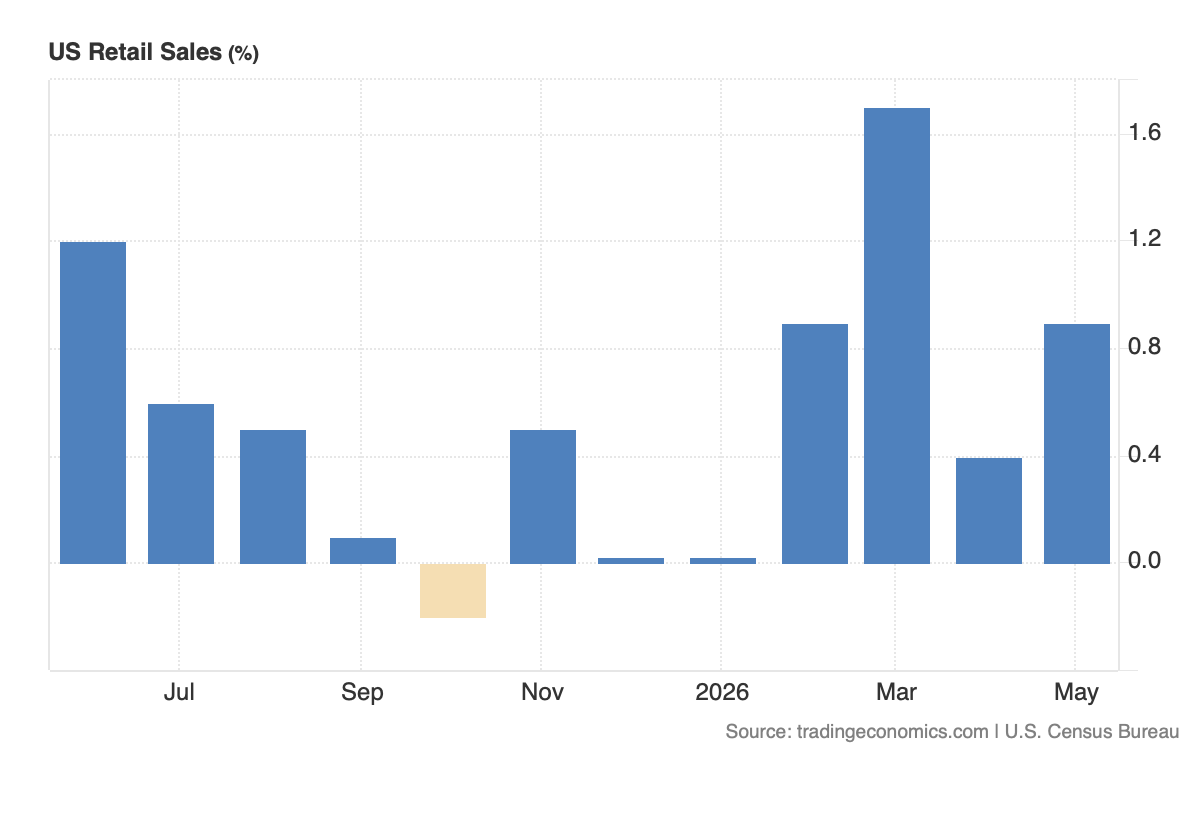

May retail and food-services sales hit $763.7 billion — up 0.9% on the month and 6.9% year over year, with the control group (the cleaner read on underlying demand) up 0.7%, according to the U.S. Census Bureau.

For us, that's the tailwind that matters. Healthy sales are the single best leading indicator of a tenant who renews, absorbs a scheduled bump without a fight, and — if you have percentage-rent clauses — pushes your effective yield higher. The backdrop for holding a well-leased center right now is good.

The one line to circle: restaurants slipped

Almost every category rose. The exception was food services, down 0.1% — the lone decliner on the month.

Here's why that line matters more to you than to almost anyone else. Restaurants are often your highest rent-per-square-foot tenants and your biggest traffic drivers — the anchor that pulls cars into the lot for the nail salon, the dry cleaner, the dentist next door. But they're also the most margin-sensitive box in your center. When the consumer tightens, people don't stop buying groceries or getting their oil changed; they cut the third dinner out.

So a soft restaurant number isn't a panic signal. It's an early-warning gauge for the F&B-heavy parts of your tenant mix. And the thing pressuring that wallet right now is sitting at the gas pump.

CRE takeaway: If your center is F&B-weighted, treat this month's restaurant dip as a cue to pressure-test those tenants now — sales-to-rent (occupancy cost) ratios, not just whether the check cleared. Healthy occupancy-cost ratios are what protect your renewals and your exit cap rate.

The swing factor: gas, oil, and the talks that just flipped

National gas has now fallen three straight weeks, to roughly $4.07 a gallon, as crude came down off its peak. Brent is off about 36% from its conflict high, and crude lost roughly 8% just this past week, with WTI around $77–78.

That pump relief is exactly what frees up discretionary dollars — the dollars that become a Friday-night dinner at the restaurant anchoring your center. Falling gas is a direct tailwind to the most fragile tenants in your rent roll.

The catch, and it's this week's news: the physical reopening of the Strait of Hormuz is underway — more than 12 million barrels crossed overnight — but the follow-up U.S.–Iran talks scheduled in Switzerland were abruptly postponed Friday, and oil ticked right back up on the headline.

Strip that down to what it means for your tenants: the gas relief currently propping up discretionary spend is not locked in. It's riding on a negotiation that just stumbled. If those talks stay stalled and pump prices climb again, the first place it shows up in your portfolio is the restaurant row we just flagged.

CRE takeaway: The chain is short and direct — oil → gas → discretionary income → your F&B tenants' sales. Right now every link points your way, but the top of the chain got less certain this week. Don't underwrite your restaurant tenants' trailing-12 sales as the new normal. Build in a scenario where pump prices reverse.

The rate backdrop: a hawkish Fed that barely touched your loan

The Fed held rates at 3.50–3.75% in Chair Warsh's first meeting — but the projections flipped hawkish. The median dot now points to a rate hike by year-end, nine of eighteen officials penciled one in, and the inflation forecast was revised up.

The headline you'll see everywhere is "rate cuts are dead." For your borrowing, that headline is mostly noise — and here's the part most owners get wrong.

Your strip center loan doesn't price off the fed funds rate. It prices off the 10-year Treasury plus a lender spread. And the 10-year sat around 4.45% this week — basically flat — because the same oil relief that's helping your tenants also pulled long rates down, even as the Fed leaned hawkish on the short end.

So the actual math: a 10-year near 4.45%, plus a retail spread of roughly 1.75 to 2.25 points, puts your loan rate around 6.2 to 6.7%. Run that against your NOI for your debt-coverage ratio, and what's left is your cash-on-cash. That range barely moved this week.

What actually changed isn't your cost of capital. It's the planning assumption. The market spent months underwriting deals to a rate cut that was supposedly coming later this year. The Fed just took that cut off the table. If your hold or refi math only works on the assumption of cheaper money arriving, that assumption is now gone — even though your real loan rate is about where it was.

CRE takeaway: Fed funds moves your tenant's credit-card rate. The 10-year moves your mortgage. Underwrite holds and refinances to today's ~6.2–6.7%, not to a cut.

What to do with this — hold, refi, or sell

If you're holding: Stress-test your F&B tenants against a gas reversal. The talks flip is your signal to do it this month, not next quarter.

If you're refinancing: Underwrite to a roughly 6.5% loan rate and a stable 10-year — not to a Fed cut. The cut is no longer in the forecast, and your lender knows it.

If you're thinking about selling "once rates drop": Understand that your buyer's financing is set by the 10-year, not fed funds — and the 10-year has been steady. A stable financing market plus a genuinely strong consumer is a cleaner backdrop to sell into than waiting on a cut that the Fed just told us may never come. Stability is a window, and it's worth more to a seller than a hoped-for cut that keeps slipping.

The waiting game changed this week. "Hold until the Fed cuts" was a strategy built on a forecast that no longer exists. But whether you hold, refi, or sell, build the plan on the rate and the consumer you can see today. Both are actually pretty constructive right now — and that's the opportunity hiding under a scary headline.

If you own a center in San Antonio, Austin, or the Rio Grande Valley and you're trying to figure out what this week actually means for your specific property, that's the conversation I have every day. Reach out — I'd rather help you think it through than have you guess.

— Ray Kang, CCIM · raycrebroker.com

WATCH OR LISTEN ON YOUTUBE ▶️(link)

Sources (June 13–19, 2026)

U.S. Census Bureau — Advance Monthly Retail Trade, May 2026 (Jun 17)

AAA / CNBC — gas prices and crude oil (Jun 14–19)

OilPrice.com / CNBC — Strait of Hormuz reopening and postponed U.S.–Iran talks (Jun 19)

Fox Business / CNBC — June FOMC decision and Summary of Economic Projections (Jun 17)

Federal Reserve H.15 / MacroMicro — 10-year Treasury (Jun 18)

The Retail Weekend Wrap-Up is market intelligence for strip center owners, not investment, legal, or tax advice.