Nobody's Building New Retail. If You Own a Strip Center, That's Your Moat.

Retail Weekend Wrap-Up — Week of June 20–26, 2026

For the better part of a decade, the headlines insisted retail was dying. They misdiagnosed the patient. What was actually failing wasn't physical retail — it was a tired model of oversized boxes and stale anchors. Fix the tenant mix, and the same real estate comes roaring back.

But there's a second story underneath that one, and it's the quieter, more durable advantage: scarcity. Almost nobody is building new retail anymore. If you already own a well-located, well-tenanted center, that scarcity isn't a problem to manage around. It's a moat.

This week handed us the three data points that make the case — a supply squeeze, a resilient consumer, and a small but real break on financing costs. Let's take them in order.

1. The supply squeeze: replacement cost is the whole story

A piece of brokerage commentary circulated this week with a framing worth keeping: the modern shopping center isn't a collection of leases — it's a curated experience, and the landlord is the merchandiser. That's the right instinct. But I want to anchor it on the mechanic underneath, because the mechanic is what protects your equity.

Here's the structural truth I'd ask every owner to internalize. New retail construction has effectively stalled, and it's stalled for a rational reason: it costs more to build a center today than most existing centers would trade for. When replacement cost sits above market value, developers don't break ground — so the supply of competing space stops growing. There's no new strip center going up across the street to undercut your rents or poach your tenants.

Meanwhile, on the demand side, e-commerce already took the business it was always going to take. The commodity, repeat-purchase categories migrated online — and then online sales plateaued. Roughly 83 cents of every retail dollar is still spent inside a physical store. The internet didn't swallow retail. It took a slice, hit its ceiling, and left the daily-needs and services business right where it always was: in your center.

Demand holding, supply frozen. In any other asset class, we'd recognize that immediately as a setup. In retail, a decade of bad headlines trained owners not to see it.

CRE Takeaway: When replacement cost is above market value, you own something that cannot be cheaply duplicated next door. That's the most underrated source of pricing power in a strip-center rent roll — it shows up as renewal leverage, lower rollover risk, and a defensible floor under value. The owners who win the next 24 months are the ones who stop managing for vacancy fear and start managing for the scarcity they already hold.

(A sourcing note, in the interest of straight talk: you'll see a "5.3%, lowest in 20 years" vacancy figure floating around in retail commentary right now. That specific number traces back to 2024 data. The current hard reads — Cushman & Wakefield had national shopping-center vacancy near 5.9% in Q1 2026, still well under the 7.4% long-run average, with a construction pipeline under 0.3% of existing inventory — tell the same supply-constrained story without leaning on a stale stat. I'd rather give you the honest version.)

2. The consumer absorbed a 4% inflation print and kept spending

Scarcity only matters if the demand behind it holds. This week we got the read, and it held.

The Fed's preferred inflation gauge, PCE, came in Thursday at 4.1% year over year — the hottest headline reading since 2023, with core PCE at 3.4%. On paper, that's a squeeze on household budgets. But look at what consumers actually did rather than what the index says they should feel: spending rose 0.7% on the month, ahead of forecast, and personal income rose 0.7% as well. The customer your tenants serve absorbed higher prices and kept walking through the door.

I'll be straight about the asterisk, because you should underwrite to it: part of that spending power came from tax-refund timing and one-off income, and that cushion fades over the coming months. This is not a green light to assume the consumer is invincible. It's evidence that right now, the needs-based and service tenants in a good center are being supported by a customer who is still spending — even while telling every survey-taker that prices are too high.

CRE Takeaway: This is the case for the tenant mix we keep returning to — necessity and services you can't download. Grocery, medtail, fitness, food, and personal care: the categories that generate repeat trips regardless of the inflation print. A 4.1% PCE headline is exactly the environment where a discretionary-heavy rent roll gets tested and a needs-based one keeps paying. If you're reviewing renewals this summer, weight your retention dollars toward the traffic-driving anchors first.

3. Cheaper money — and what it does to your deal math

The financing picture got marginally friendlier this week, and it's worth translating into your numbers rather than leaving it as a bond-market abstraction.

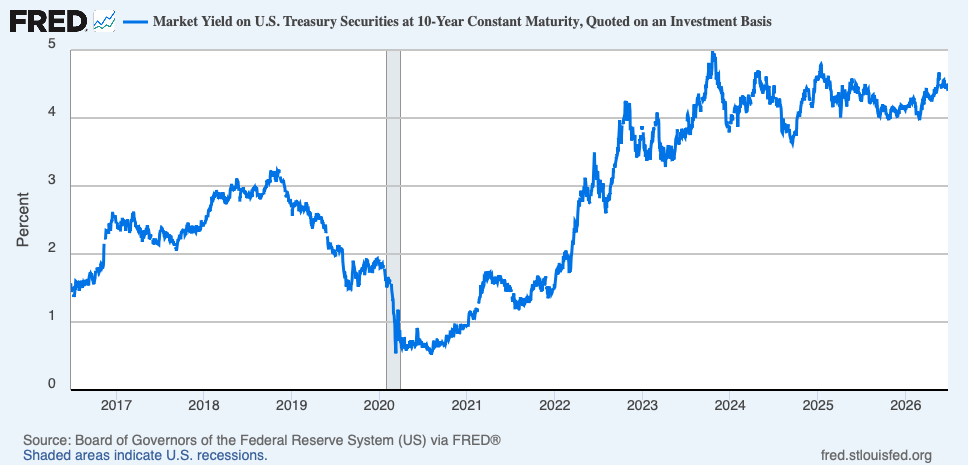

The 10-year Treasury — the base rate your lender prices off of — drifted down to about 4.38%, near a seven-week low, after the in-line inflation read let markets trim some rate-hike bets. At the same time, the national gas average slipped back under $4 to roughly $3.90, with Texas among the cheapest states near $3.36 a gallon. Cheaper fuel puts a little more discretionary room back into your shoppers' wallets — a small tailwind for the same tenants we just discussed.

Here's the mechanic, in plain language. Your loan rate isn't the 10-year — it's the 10-year plus a lender spread, which on retail is running roughly 175 to 225 basis points right now. Stack that on a ~4.38% base and you land in the low-to-mid 6% range for a typical strip-center loan today. From there the chain is simple: loan rate sets your debt service; debt service measured against NOI sets your debt-coverage ratio (DCR); and what's left after debt service, divided by your equity in the deal, is your cash-on-cash return.

This week's move was small — about 7 basis points. On a $3.25 million loan, that's roughly $2,300 a year in interest. Not decisive on its own. But direction is the story. If you've been sitting on a refinance, or waiting to underwrite an acquisition, a 10-year drifting toward the low 4s is the difference between deals that pencil and deals that don't.

CRE Takeaway — the deal-math frame: 10-Year Treasury (~4.38%) + lender spread (~175–225 bps) = loan rate (~low-6%). Then loan rate → debt service → DCR → cash-on-cash. Don't anchor to a composite cap-rate headline; anchor to your borrowing cost, because that's what actually clears or kills the deal. If you want your specific center run through this framework — current debt, NOI, and equity — that's a short conversation and worth having while the 10-year is cooperating.

The Strait of Hormuz

4. The caveat: don't bank the relief yet

One honest caution before we close, because the rate relief above is leaning on cheaper oil — and that piece isn't fully settled.

Oil had been sliding all month as shipping through the Strait of Hormuz began to normalize. But late this week, prices ticked back up after a cargo vessel was struck near the Omani coast and a planned evacuation of stranded ships was paused. Treat it strictly as a supply-and-price signal: the relief trade in energy — and therefore in inflation, and therefore in your borrowing costs — is real but fragile. Analysts expect it could take weeks to months for shipping flows to fully return.

CRE Takeaway: Underwrite the relief as a window, not a new baseline. If a refinance pencils at today's rate, the prudent move is to act inside the window rather than wait for a lower number that depends on a fragile energy story holding. Lock what works; don't speculate on what might come.

The week in one breath

The consumer is still spending through a 4% inflation print. Money got a touch cheaper. And the supply of competing retail space is frozen solid. The macro is the tailwind. The scarcity is the moat.

If you own a quality center, you're not waiting for the market to come back. You're holding the one thing the market can't make more of. The job now is to merchandise it like the asset it is — and to know your number before the window moves.

If you want to know what your center is worth in this market, or whether a refinance pencils today, reach out. That's what I do all week, across San Antonio, Austin, and the Rio Grande Valley.

— Ray Kang, CCIM StripCenterIQ

WATCH OR LISTEN ON YOUTUBE ▶️ @raycrebroker