Higher-for-Maybe: Why a Weak Jobs Report Won't Cut Your Strip Center's Rate

A note before the market read. Today marks 250 years of America — two and a half centuries of people betting on a storefront and a piece of ground they could own and build on. That's the story of every strip center we work in: local businesses, family owners, Main Street leased up one deal at a time. Grateful to spend this work alongside the Texas owners who keep it open. Happy 250th.

For two years, the strip center playbook has rested on a single quiet assumption: rates are high now, but relief is coming. Hold on, refinance later, sell into a world of lower cap rates. This week, the data pulled that assumption out from under us — and if your strategy depends on rate relief, this is the week to re-examine it.

A weak report that buys no relief

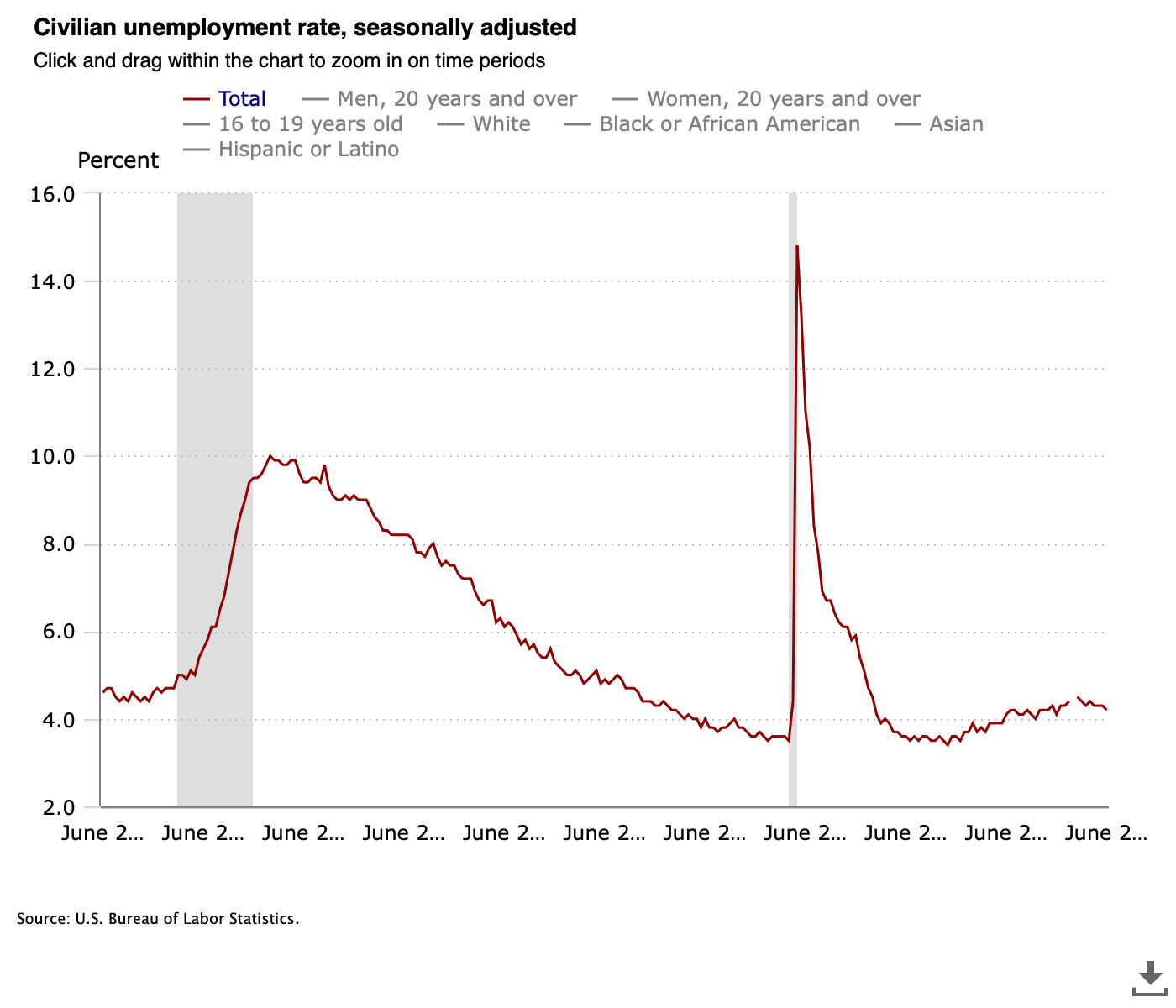

June payrolls came in at just 57,000, well under the roughly 115,000 consensus. The headline unemployment rate fell to 4.2%, but the detail tells a different story: labor force participation dropped to 61.5%, the lowest reading since March 2021, and the household survey recorded about 507,000 fewer people working. Layer in 74,000 of downward revisions across April and May, and a 61,000-job decline in leisure and hospitality, and this is a genuinely soft month.

In an ordinary cycle, that is the setup for rate cuts, cheaper debt, and cap-rate compression. This is not an ordinary cycle. The Fed removed its easing bias in mid-June, its Chair stated plainly that “prices are too high,” and the market is now pricing a roughly 50-to-60 percent chance of a rate hike in September. With inflation still running near 4%, the Fed has decided that is the fire it is fighting — not the labor market.

🔗 Sources: BLS Employment Situation — June 2026 · Fed rate pricing (CNBC)

You're watching the wrong part of the curve

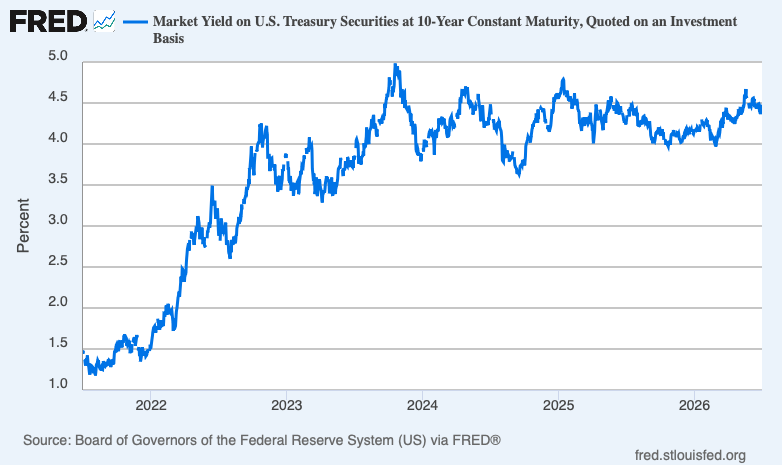

Here is the trap most owners fall into. The soft jobs number did move rates — but it moved the short end. The 2-year Treasury fell to 4.14%. The 10-year, which is what your strip center debt actually prices off, barely budged and closed at 4.49%. The instinct that “a bad jobs number means cheaper loans” is, this cycle, watching the wrong part of the curve.

Run the arithmetic. Your loan rate is a base rate plus a lender spread. The base rate is the 10-year at about 4.49%. On a quality retail strip center, lenders are adding roughly 1.75 to 2.25 points, which puts financing in the 6.25% to 6.75% range. That loan rate drives your debt service, your debt coverage ratio, and ultimately your cash-on-cash return. None of those numbers improve if you simply wait. For a year, waiting was a strategy — you were waiting for the base rate to fall. This week the Fed signaled it could go the other way. Waiting is no longer a free option.

🔗 Source: 10-Year Treasury, DGS10 (FRED)

The tenant side of a slowing labor market

Step back and think like a landlord. A cooling labor market combined with inflation near 4% squeezes the household budget from both directions, and it does not hit every tenant equally. The most exposed categories are discretionary: full-service restaurants, boutique fitness, specialty apparel. The categories that hold up are essentials and value — grocery, medical, quick-service food, discount and service tenants. That divide is precisely why grocery-anchored and service-heavy strip centers have remained the most defensive product in the market.

Across San Antonio, Austin, and the Rio Grande Valley, those fundamentals are still firm: quality centers are full, second-generation space draws multiple looks, and private buyers are competing hard for good income. But this is the quarter to pull your rent roll and ask which tenants sit on the discretionary side of that line, and when their leases expire.

Three doors: hold, refinance, sell

For most owners, this comes down to three doors, and the right one depends entirely on your debt and your timeline.

Hold and ride. If your debt is fixed, long-dated, and your center is well-tenanted, holding through the rate fog is defensible. Underwrite it honestly — assume the 10-year stays above 4.5% and your eventual refinance lands in the high-6s. If the hold still works on those assumptions, hold with confidence.

Refinance now. If a maturity is coming inside the next 12 to 18 months, this week changed the calculus. Locking today, before a possible September hike, may well beat waiting for relief that is no longer on the schedule.

Sell. If your hold thesis quietly depended on rates falling, it needs a hard second look. Private-buyer demand for quality Texas strip income is still deep, the best product still trades at sub-7 caps, and supply is thin. Selling into that demand now may capture more than waiting for a cut the Fed just told you it isn't planning.

Higher-for-longer assumed the next move was down. Higher-for-maybe means it could be up — and your strategy cannot rest on relief that isn't scheduled. Whichever door you choose, choose it on today's rate reality.

If you own a strip center in San Antonio, Austin, or the Rio Grande Valley and you're not sure which door is yours, that's the work I do every day — a straight read on your specific property and your specific debt. Reach out anytime.

Across platforms: Watch on YouTube · Read on LinkedIn · Subscribe on Beehiiv