One Waterway Away: What 4.2% Inflation, a Record PPI, and the Iran Deal Mean for Your Strip Center

Retail Weekend Wrap-Up | June 13, 2026

Four point two percent.

That's the inflation number the Bureau of Labor Statistics published on Wednesday morning — the highest annual rate in the United States in three years. If you own commercial real estate, that number probably got your attention. It should.

But this week I want to open the hood on it. Because when you take the report apart, the story underneath is very different from the headline — and the gap between the two is exactly the difference between panicking about your strip center and positioning it.

This week gave us the May inflation report, the May producer price report, a 10-Year Treasury that did something almost nobody expected, three straight weeks of falling gas prices, and a war that may be days from ending. All of it connects. Let's get into it.

CPI: The 4.2% Isn't What You Think

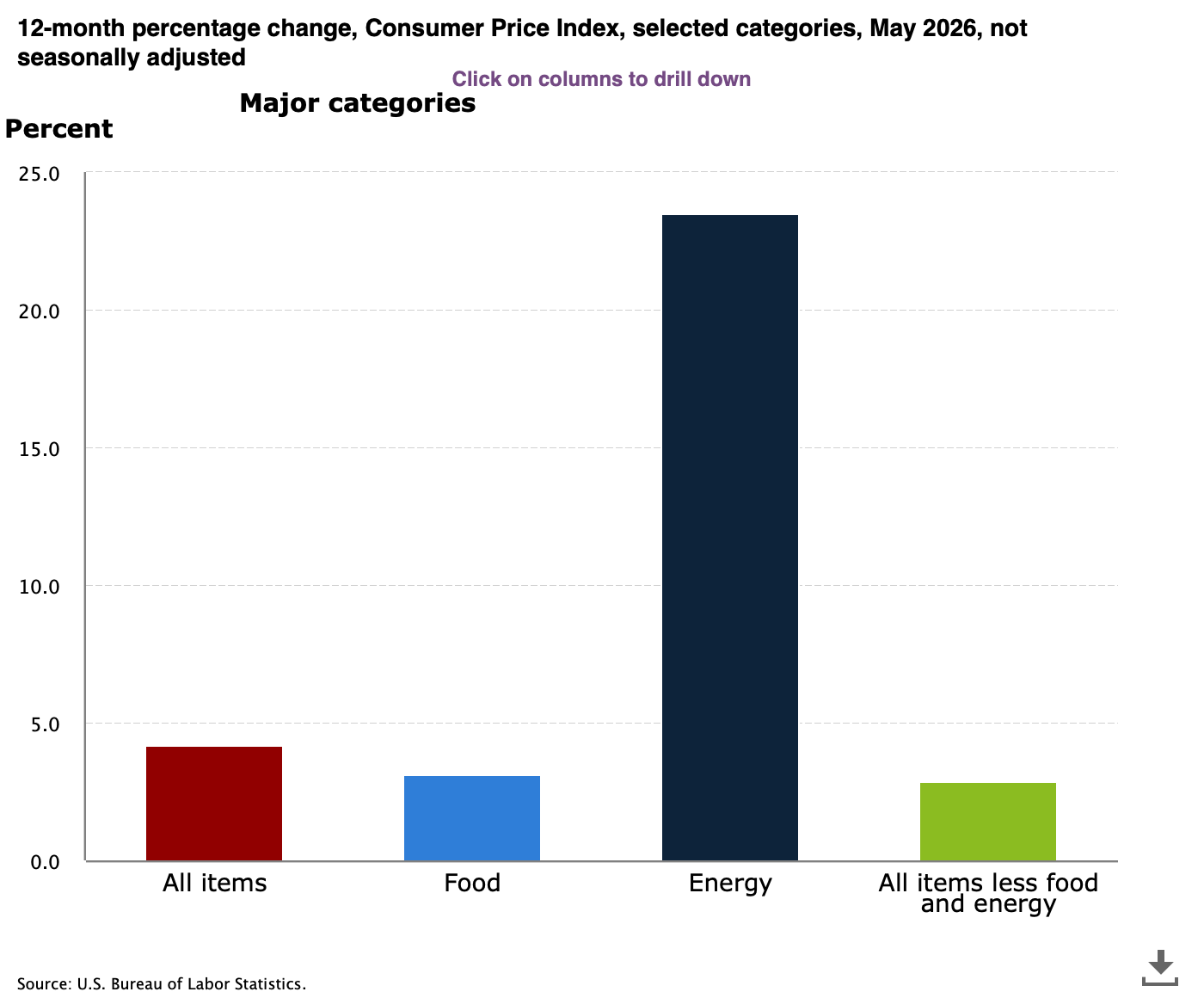

The BLS reported that consumer prices rose 0.5% in May and are up 4.2% over the past year — the hottest annual reading since April 2023.

Here's the part that matters: energy accounted for over 60% of the entire monthly increase. Energy prices rose 3.9% in May alone and are up 23.5% over the past year. Gasoline jumped 7% in a single month and is up more than 40% from a year ago. That is the Iran war showing up at the pump and in the index.

Now strip out food and energy and look at core inflation — the measure the Federal Reserve actually steers by. Core CPI rose just 0.2% in May, below forecasts, and sits at 2.9% annually. Core goods prices actually declined.

The inflation fire is burning in one room of the house — energy. It is not spreading through the structure.

That distinction matters in two directions for a property owner. Your tenants' customers feel the 4.2%, because gas, groceries, and electricity are the prices people encounter every week — so expect the value-conscious consumer to remain value-conscious. But lenders and the bond market price off core, and core is the calmest part of this entire report. That's why your borrowing costs didn't blow out this week, which we'll get to shortly.

PPI: What's Building Upstream

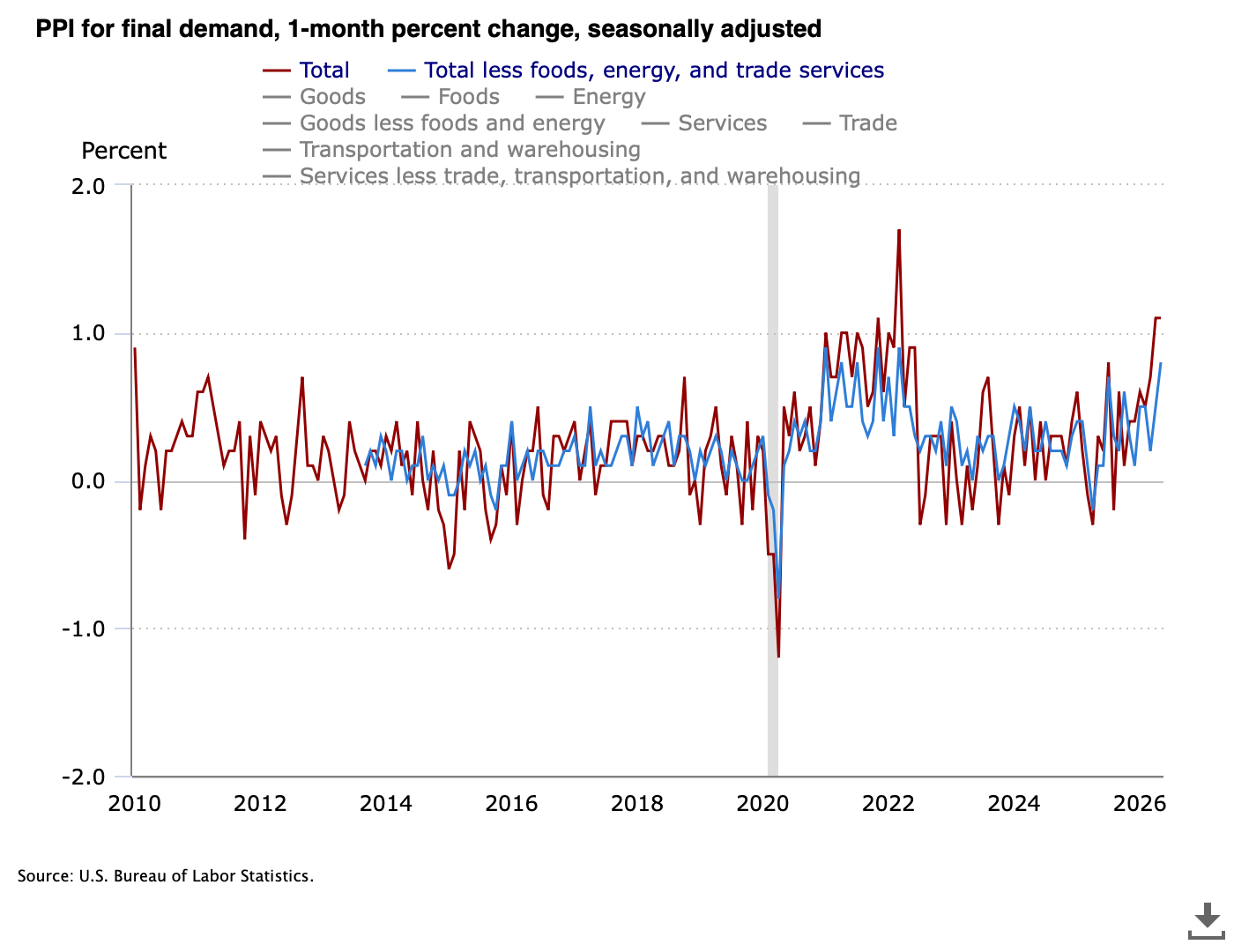

One day after CPI, we got the Producer Price Index — what businesses pay before costs ever reach a consumer. This one ran hotter: producer prices for final demand rose 1.1% in May and are up 6.5% over the past year, the largest annual increase since November 2022.

The detail I keep coming back to is what the BLS calls stage 1 intermediate demand — the rawest inputs at the very start of the production pipeline. That index jumped 3.2% in May, the largest one-month increase since the government began calculating the series in 2009. It's up 12.3% over the past year. Diesel, jet fuel, industrial chemicals — the energy shock is loading cost pressure into the pipeline.

Why does that matter for the second half of the year? Because pipeline costs don't stay in the pipeline. If the war drags on, those upstream costs work their way downstream into freight, into construction materials, into your tenants' cost of goods — and eventually into the consumer prices the Fed has to respond to. If the war ends, much of that pressure decays before it ever arrives.

Two practical notes for owners. First, if you're pricing a capital project this summer — a roof, a parking lot, a facade package — the bids you receive ride this same pipeline. Second, it's worth asking your restaurant and service operators how their input costs are tracking. Their margins feel PPI months before your rent roll does.

And one footnote for the data-minded: buried in the same report, gross rents for retail properties appeared among the declining price indexes in May. One month is not a trend. But it's a data point worth knowing exists, and worth watching.

The Week the War Turned

Everything above traces back to one place: the Strait of Hormuz, closed since the U.S.–Iran conflict began in late February. Roughly a fifth of the world's oil moves through that waterway in normal times. America's inflation problem in 2026 is, at its core, an energy problem — and the energy problem is one waterway wide.

This week, that story moved. On Thursday, President Trump said the war was, in his words, basically settled — and that an agreement could be signed within days. Oil fell hard on the news: Brent dropped as much as 5% to its lowest level since the early days of the war in March. By Friday, Iranian state media had published what it described as a draft agreement. The President disputed that the published text matched what had been negotiated — but Pakistan's prime minister, who has mediated the talks, confirmed that a final agreed text has been reached. The core of the deal: reopening the Strait of Hormuz. As of Friday, WTI crude sat near $84.76 and Brent near $87.44, both down again on the day.

A dose of humility is in order. Markets have heard near-deal signals repeatedly since March, and no agreement has been signed. But this week was different in one respect: it's the first time the optimism arrived alongside a mediator confirming an agreed text. The bond market noticed. So did the pump.

On that note: AAA reported Thursday that the national gas average fell for a third consecutive week to about $4.11 a gallon — down from the peak of $4.55 in late May. Texas drivers typically pay below the national average, and falling fuel prices are the most direct relief your tenants' customers can get. Every dollar not spent on gas is a dollar available at the wing shop, the nail salon, and the taqueria in your center.

The scenario planning writes itself. If the deal signs, energy prices decay, headline CPI rolls over in the second half, the consumer gets a real raise at the pump, and the rate conversation softens — constructive for leasing velocity and deal flow. If the deal stalls, that record pipeline pressure flows into consumer prices through the fall and the Fed conversation gets harder. Either way, the move for an owner is the same: position your center for the consumer who exists today — value-conscious, necessity-driven, and still showing up.

Why the 10-Year Shrugged at a Three-Year Inflation High

Here's the moment that tells you what the smart money believes.

The hottest CPI print in three years landed Wednesday morning — and the 10-Year Treasury barely moved, holding around 4.55%. Then on Thursday, as the peace signals firmed up, the 10-Year fell roughly 10 basis points. It ended the week near 4.47%.

Think about what that means. The bond market looked at a 4.2% headline and decided it was not the real story — because core was tame, and because the energy driver may be days from reversing. If bond investors believed this inflation were durable, yields would have surged. They didn't.

Now the deal math, because this is where it lands on your property. Retail centers are financing today at roughly the 10-Year plus 175 to 225 basis points of lender spread. At 4.47% on the 10-Year, that puts loan quotes in the range of roughly 6.2% to 6.7%. That's not cheap money — but it's stable money, and stability is what gets deals underwritten and closed.

If you've been waiting for rate clarity before refinancing or taking your property to market, understand what a signed agreement would represent: the clearest directional signal this market has produced all year. Have your numbers ready before the headline, not after.

Control What You Can Control: Medtail as the Defensive Anchor

Everything to this point is outside your control. You don't set oil prices. You don't negotiate with Iran. You don't vote on the FOMC. But there is one lever that's entirely yours — and it's the most powerful one in this whole story: who pays you rent.

This week, CoStar published a conversation with JLL's U.S. healthcare lead, Matt Coursen, on a migration that's been reshaping retail real estate: healthcare services are steadily moving out of traditional hospital campuses and into outpatient facilities closer to where patients live — which increasingly means retail real estate. Hospital systems want their expensive on-campus space backfilled with high-value services, and they want routine care out in the neighborhoods.

In my markets — San Antonio, Austin, and the Rio Grande Valley — I see this every week, and I'll tell you what it looks like from the advisory side of the table. The urgent care, the dental group, the physical therapy clinic, the imaging center, the vet — these are the tenants competing for endcaps and inline space in well-located strip centers. And they behave differently than almost any other tenant category.

They're sticky. A medical tenant doesn't sink six figures into plumbing, electrical, and buildout and then relocate over fifty cents a foot at renewal. Their tenant improvement investment anchors them to your address, and their patient base anchors them to your trade area.

They're credit. National medical platforms bring institutional-grade covenants, and even independent local practices typically post stronger financials than an independent restaurateur.

And they're traffic. Medical visits are booked, recurring, midweek, daytime traffic — the highest-quality footfall your other tenants can ask for. The patient who comes in for a 10 a.m. appointment picks up coffee on the way in and lunch on the way out.

Here's the tie back to everything else this week: medtail demand doesn't move with gas prices. Nobody cancels a root canal because crude went up. In a year where the macro story changes by the headline, healthcare-anchored income is the closest thing to inflation-resistant cash flow a strip center owner can build.

One caution from the advisory side: medtail leases carry real diligence items — heavier tenant improvement negotiations, parking intensity, utility sub-metering, restoration clauses at lease end. The economics are some of the best in retail leasing, but the lease itself deserves more scrutiny, not less. Get advice before you sign, not after.

And if you're thinking about an eventual sale, know this: a buyer underwriting your center pays for durability. A rent roll built on medical, service, and food tenants on long terms is worth more than the same NOI from discretionary retail — and the spread between those two valuations is widening.

The Bottom Line

The scariest inflation number in three years turned out to be a war story, not a demand story. The bond market knew it — that's why your borrowing costs ended the week lower, not higher. The pipeline data says the second half of 2026 depends on whether one waterway reopens. None of that is in your control.

What is in your control is the durability of your income. The owners who come through this stretch strongest won't be the ones who predicted the headlines — they'll be the ones whose rent rolls didn't care what the headlines said.

WATCH OR LISTEN ON YOUTUBE ▶️

If you own a strip center in San Antonio, Austin, or the Rio Grande Valley and want a second set of eyes on your tenant mix, your lease maturities, or what your property would command in today's market — reach out. That conversation costs you nothing, and it's the part of this I do every day.

Ray Kang, CCIM, is a commercial real estate investment sales advisor specializing in retail strip centers across San Antonio, Austin, and the Rio Grande Valley.

Sources

U.S. Bureau of Labor Statistics — Consumer Price Index, May 2026 (released June 10, 2026): https://www.bls.gov/news.release/cpi.nr0.htm

U.S. Bureau of Labor Statistics — Producer Price Index, May 2026 (released June 11, 2026): https://www.bls.gov/news.release/ppi.nr0.htm

CNBC — 10-Year Treasury Yield Steady After Inflation Data (June 10, 2026): https://www.cnbc.com/2026/06/10/us-treasury-yields-inflation-data.html

CNBC — Oil Prices Fall on Proposed U.S.–Iran Deal (June 12, 2026): https://www.cnbc.com/2026/06/12/oil-prices-wti-brent-on-hopes-of-us-iran-deal-despite-tehran-pushback.html

AAA Newsroom — Pump Prices Fall for Third Straight Week (June 11, 2026): https://newsroom.aaa.com/2026/06/pump-prices-fall-for-third-straight-week/

CoStar News — Four Questions for Healthcare Real Estate Pro (June 9, 2026): https://www.costar.com/article/2014368151/four-questions-for-healthcare-real-estate-pro-land-constrained-medical-systems-should-think-vertically

FRED, Federal Reserve Bank of St. Louis — 10-Year Treasury Constant Maturity (DGS10): https://fred.stlouisfed.org/series/DGS10