The Exhale: When Relief Is Not Recovery

Retail Weekend Wrap-Up, April 18, 2026

This week, the market held its breath, then finally exhaled. Gas prices came down. Mortgage rates fell to a four-week low. Oil plunged more than 11% in a single session on Friday. The S&P 500 and Nasdaq both closed at record highs. And Ares Management signed a definitive agreement to take Whitestone REIT private for $1.7 billion — a Houston-based shopping center REIT with substantial holdings in San Antonio, Austin, and Dallas-Fort Worth.

And then by Saturday morning, the Strait of Hormuz was "back to its previous state."

Here's what strip center owners need to internalize before they act on any of this: an exhale is not a recovery. Sometimes it only lasts until the next morning. A two-week ceasefire is not a treaty. A one-day rally in crude is not a solved problem. And the damage to the consumer psyche from the last six weeks doesn't repair overnight.

Here is what happened this week, and what it means for your portfolio.

Gas Prices: The First Sign of Relief in Six Weeks

The 36-Hour Whipsaw at the Strait of Hormuz

Let's start with oil, because this story moved twice in 36 hours, and what happens next in the Persian Gulf will shape everything downstream for strip center owners.

Friday morning, Iran's foreign minister declared the Strait of Hormuz "completely open" for commercial vessels, citing the Israel-Lebanon ceasefire. Markets reacted immediately and dramatically. WTI crude plunged 11.4% to $83.85 per barrel — its lowest level since March 10 and the second-largest single-day drop since the war began in late February. Brent fell 9%. The S&P 500 and the Nasdaq both closed at record highs — their third consecutive record closes. The 10-year Treasury yield fell to 4.24%, its lowest since March 18.

Then this morning — Saturday — Iran reversed. Iranian military officials announced that the Strait has "returned to its previous state" and is once again under "strict management and control," citing the ongoing U.S. blockade of Iranian ports that began Monday, April 13. Two Iranian gunboats reportedly fired on a tanker roughly twenty nautical miles northeast of Oman this morning. The U.S. says twenty-three ships have been turned back since its blockade started five days ago.

The single most important piece of context behind all of this: the two-week U.S.-Iran ceasefire expires this coming Tuesday, April 21 — three days from when you are reading this. Islamabad peace talks broke down earlier this week. President Trump told reporters a second round of negotiations would "probably" happen this weekend, but U.S. officials privately view Monday as the earliest feasible date. The single most important variable in global energy prices — and therefore in your tenants' discretionary spending picture — is a political negotiation that has not yet started and faces a deadline 72 hours from now.

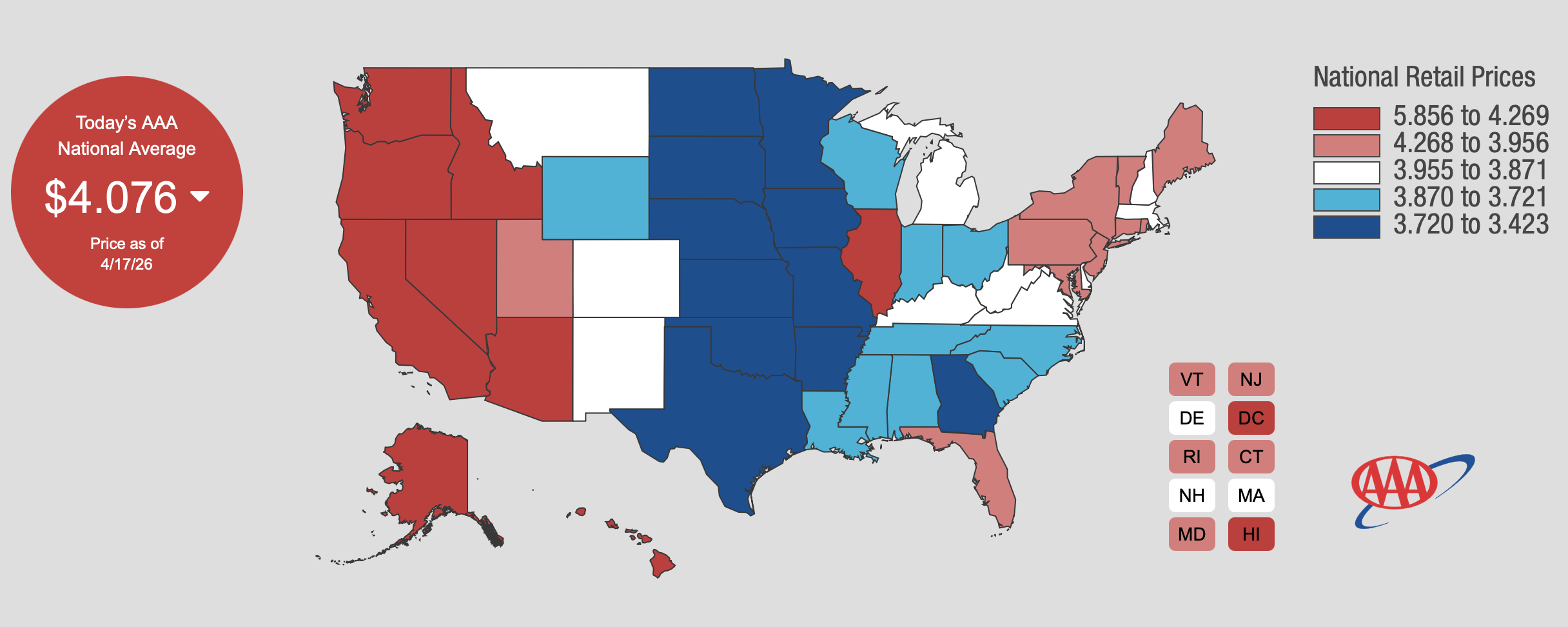

On the gas pump, the most recent hard data is AAA's Wednesday release, which showed the national average for regular gasoline fell seven cents over the past week to $4.09 per gallon — the first weekly decline since the conflict began in late February. Important context: the national average on February 26 was $2.98. Even after the recent drop, pump prices remain approximately 37% higher than they were six weeks ago. The ceasefire helped. Today's Hormuz reversal will slow the rate of decline. And depending on what happens in the next 72 hours, next week's pump price could move in either direction.

For strip center owners, the relevance is direct and material. Higher pump prices pull discretionary dollars away from the tenants that anchor most suburban retail rent rolls — the nail salons, quick-service restaurants, tutoring centers, local apparel, and specialty services that depend on household disposable income. When a household's weekly gas bill jumps from $60 to $85, something else gets cut. That something is often the Saturday lunch, the mid-week manicure, or the impulse stop at the local boutique.

The question this week is no longer whether one week of gas relief will restart tenant foot traffic. It won't, not by itself. The better question is whether the ceasefire holds long enough for households to recover budget breathing room — and whether tenants can survive the interim if it doesn't.

Ask your tenants, directly and soon, how traffic looked the last two weeks of March compared to the first two weeks of April. That comparison is your leading indicator for how the energy shock is translating into your rent roll. And don't underwrite any scenario that assumes gas prices keep falling linearly from here.

Mortgage Rates Hit a Four-Week Low

Mortgage Rates Hit a Four-Week Low

Freddie Mac's Primary Mortgage Market Survey released Thursday showed the 30-year fixed rate fell to 6.30%, down from 6.37% last week — a four-week low and meaningfully below the 6.83% we were looking at a year ago.

What's driving the move is the 10-year Treasury yield, which fell Friday to 4.24% — its lowest level since March 18 — after the Hormuz open announcement. Bond investors repriced inflation risk downward on the news. Oil-driven inflation fears eased, money flowed back into Treasuries, yields fell, and mortgage rates followed. Some portion of that move likely gets given back Monday morning when markets open and reprice the Hormuz reversal. How much depends on what happens over the weekend. The key point: today's rate sheet and Monday's rate sheet are not the same piece of paper.

This matters for residential real estate directly. But strip center owners need to translate the movement to commercial loan pricing, because the mechanics are different.

Small-balance commercial real estate loans typically price off the 5-, 7-, or 10-year Treasury plus a spread of roughly 200 to 275 basis points, depending on sponsor quality, tenant credit profile, loan-to-value, and lender. A 10-basis-point move in the benchmark does not flow one-for-one to your CRE loan, but on a refinance across a $5 million to $15 million strip center, it is real money.

Consider a concrete example. On a $5 million loan with a 25-year amortization, moving the rate from 6.75% to 6.50% reduces annual debt service by roughly $8,000. That sounds modest. But if your deal is underwriting to a 1.25 debt coverage ratio, that $8,000 restores approximately $10,000 of effective annual NOI cushion for the lender. On a borderline deal, that can be the difference between approval and denial — or between full proceeds and a haircut.

The actionable posture here is straightforward. If you have a loan maturing in the next 6 to 12 months, call your mortgage broker Monday morning — not next week. Get a live quote. Run scenarios against current pricing. The window that opened Friday can close as fast as it opened, and given the Hormuz whipsaw, "fast" now means hours rather than weeks. Peace talks could still land constructively, in which case rates stay soft. Or the ceasefire could collapse Tuesday, in which case Friday's rate sheet was the floor and what comes next is higher.

A two-week ceasefire is not a trend. Be ready to move.

Ares Buys Whitestone REIT for $1.7 Billion — In Our Backyard

Ares Buys Whitestone REIT for $1.7 Billion — In Our Backyard

The most important CRE news of the week did not come from Washington or Wall Street. It came from a Houston-based real estate investment trust and a New York private equity firm.

On April 9, Ares Management Corporation and Whitestone REIT announced a definitive merger agreement valued at approximately $1.7 billion. Ares will acquire all outstanding Whitestone common shares and operating partnership units for $19.00 per share or unit in an all-cash transaction. The purchase price represents a 12.2% premium to Whitestone's closing stock price on April 8, 2026, and a 26.5% premium to the unaffected share price before a March 5 Reuters article reported the company had engaged advisors to explore a sale. The deal is expected to close in the third quarter of 2026.

What makes this news directly relevant to strip center owners in Texas and the broader Sun Belt: Whitestone's portfolio comprises 56 convenience-focused retail properties totaling approximately 4.9 million square feet — with substantial holdings concentrated in San Antonio, Austin, Houston, Dallas-Fort Worth, and Phoenix. This is not a coastal REIT deal with a tangential relationship to our markets. This is institutional capital writing a $1.7 billion check for the exact product type and geography many of our clients own.

The deal also came with a backstory worth pausing on, because the lesson it contains is as valuable as the transaction itself.

MCB Real Estate, a Baltimore-based private equity firm, spent more than eighteen months trying to acquire Whitestone. MCB made an initial offer of $14.00 per share in June 2024. It was rejected. MCB returned with $15.00 per share. Also rejected. In November 2025, MCB publicly bumped its offer to $15.20 per share in cash with no financing contingency. Again rejected. Throughout the process, the Whitestone board declined to grant due diligence, engage in meaningful negotiations, or initiate a strategic alternatives process.

Then, on April 15, 2026, MCB publicly withdrew its proposal, blasting what it described as the Whitestone board's intransigence and entrenchment. But by that date, the board had already engaged with Ares and signed a definitive agreement at $19.00 per share. The board that refused to negotiate at $15 ultimately delivered shareholders $19. That is $3.80 per share higher than the most recent MCB bid — real money at Whitestone's share count.

There are three messages here that strip center owners should internalize.

First, sophisticated institutional capital believes convenience-focused, necessity retail in Sun Belt growth markets is a buy at today's cap rates. Ares's global head of real estate strategy described the thesis in terms of retail markets with high demand and low supply pipelines — precisely the Sun Belt thesis that private strip center owners have been executing for years. When a firm of Ares's scale writes a $1.7 billion check for 56 centers in our markets, they are not predicting a recovery next quarter. They are pricing durable cash flow over a ten-plus-year hold.

Second, the deal repriced the public-market discount. Whitestone was trading roughly 26.5% below its unaffected takeout price before the sale process became public. That tells you sophisticated buyers view public REIT shares in the strip center category as materially undervaluing the underlying real estate right now. For private owners, the implication is that the buyer-universe conviction in your product type is stronger than public-market share prices alone would suggest.

Third, and this is the part most owners miss — the MCB saga is a cautionary tale. The Whitestone board held out for eighteen months at $15 and below. When genuine engagement finally happened, the price went to $19. Sometimes the right answer is to run a process. Sometimes the cost of entrenchment is real money left on the table. This is not a recommendation to sell. It is a recommendation to gather information. Owners who refuse to understand what their property would fetch today are not being disciplined — they are guessing.

For private owners of well-tenanted, convenience-focused strip center product in Texas or the broader Sun Belt, this week's deal is a data point worth filing carefully. If you have been considering a disposition in the next 12 to 24 months, now is a reasonable moment to commission a broker opinion of value and understand precisely where your property prices in today's market. The number may come in closer to Ares's implied thesis than you expect — or further from it. Either way, you are making your next decision with information rather than assumption.

Restaurants: $1.55 Trillion on a Fragile Foundation

Restaurants: $1.55 Trillion on a Fragile Foundation

The National Restaurant Association released its 2026 State of the Industry Report with a headline projection of $1.55 trillion in total foodservice sales this year, up from $1.4 trillion in 2025.

The headline number is strong. The structure beneath it is fragile.

Only 42% of operators were profitable last year. Sixty percent said business conditions deteriorated in 2025. More than nine in ten flagged food, labor, insurance, and overall inflation as significant challenges. And more than six in ten reported declining traffic.

The industry is growing in dollars — and most of that growth is menu price increases rather than volume. Traffic is flat to down. Margins are compressed. That is a fragile structure for an industry that represents a meaningful share of most suburban strip center rent rolls.

For landlords, the translation is important. Your restaurant tenants are not automatically weak, but they are not recession-proof either. The operators with strong unit economics, real pricing power, and discipline around food and labor costs will keep their doors open through this cycle. The ones who depended on cheap debt, low input costs, and steady traffic to break even are the ones who warrant closer monitoring.

Look at tenant sales reports. Look at rent coverage ratios. Look at how your operator has moved menu prices — faster or slower than local competitors signals pricing power. A restaurant tenant paying $35 per square foot at a 9% rent-to-sales ratio is in a fundamentally different position than one at 14%. If you don't have recent sales reports on file, request them. Most leases allow landlord access on reasonable notice. If a tenant refuses to provide them, that refusal is information in itself.

The restaurant industry is growing in dollars and shrinking in operators. Know which side of that trend your tenants are on before you need to.

The Posture for Strip Center Owners

Let's bring all four threads together.

Gas prices down seven cents. Mortgage rates at a four-week low. Oil down 11% in a single session Friday. Stocks at record highs. A $1.7 billion take-private of a Sun Belt strip center REIT with half its portfolio in Texas. A fragile but large-dollar restaurant industry at $1.55 trillion. This was a real relief rally.

And then by Saturday morning, the Strait of Hormuz was "back to its previous state." Ships were getting fired on. The ceasefire expires Tuesday, April 21. The talks have not started.

That is the cleanest illustration available of why an exhale is not a recovery. The market did not misread the news on Friday. It read it correctly, for Friday. But the situation changed in 36 hours. Consumer sentiment is still at a 74-year low. Retail store closures are still tracking toward 7,900 for the year. Restaurant operators are still running on thin margins. None of that was repaired by one good day in crude.

The correct posture for strip center owners right now is cautiously constructive.

Acknowledge the relief where it is real. Use the rate window to refinance if you can — and move fast, Monday rather than next week. Get broker opinions of value on assets you have been considering selling. Check in with your tenants about their April traffic. Pull sales reports. Model scenarios.

But do not confuse a one-day data point with a trend. And do not confuse a Friday rally with a solved problem. Stay underwriting conservative. Stay close to your assets. Stay skeptical of anyone telling you the coast is clear.

If you own a strip center in San Antonio, Austin, or the Rio Grande Valley and want to talk through what this week means for your specific property — your rate, your tenants, your hold-period strategy — reach out. That's what I do.

Ray Kang, CCIM StripCenterIQ · raycrebroker.com

WATCH OR LISTEN ON YOUTUBE ▶️

If you own a strip center in San Antonio, Austin, or the Rio Grande Valley and want to talk through what this week means for your specific property — your rate, your tenants, your hold-period strategy — reach out. That's what I do.

Ray Kang, CCIMStripCenterIQ · raycrebroker.com

Sources

NBC News — Oil prices plunge as Hormuz opens (Apr. 17, 2026)NBC News — Iran reverses, Hormuz returns to "strict control" (Apr. 18, 2026)AAA Gas Prices — National Average Falls to $4.09 (Apr. 16, 2026)Freddie Mac PMMS — 30-Year Fixed 6.30% (Apr. 16, 2026)U.S. Department of the Treasury — Daily Treasury Par Yield CurveGlobeNewswire / Whitestone REIT — Whitestone to Be Acquired by Ares for $1.7 Billion (Apr. 9, 2026)Commercial Observer — Ares Management Acquires Whitestone REIT in $1.7B All-Cash DealAGM Commercial / Bisnow — MCB Withdraws Whitestone Acquisition Proposal (Apr. 15, 2026)Restaurant Business Online — NRA 2026 State of the Industry Report (Feb. 12, 2026)