The Squeeze Becomes Structural — but Strip Centers Aren’t Buying It

Retail Weekend Wrap-Up | Week ending April 25, 2026

By Ray Kang, CCIM

This week tested every assumption strip center owners have been working with for the past six months.

On Friday morning, the University of Michigan reported that consumer sentiment hit the lowest reading on record going back to 1952. On Wednesday afternoon — barely 36 hours earlier — the largest publicly-traded grocery-anchored shopping center REIT in the country reported new lease rent spreads of 36 percent.

If you own a strip center, that disconnect is the most important thing happening in your market right now. The macro headlines and the leasing comps are screaming completely different things at each other. Both data sets are real. Both are actionable. Neither tells the whole story on its own.

Let’s walk through what happened, what it means, and what to do about it.

The Macro Tape Is Genuinely Difficult Right Now

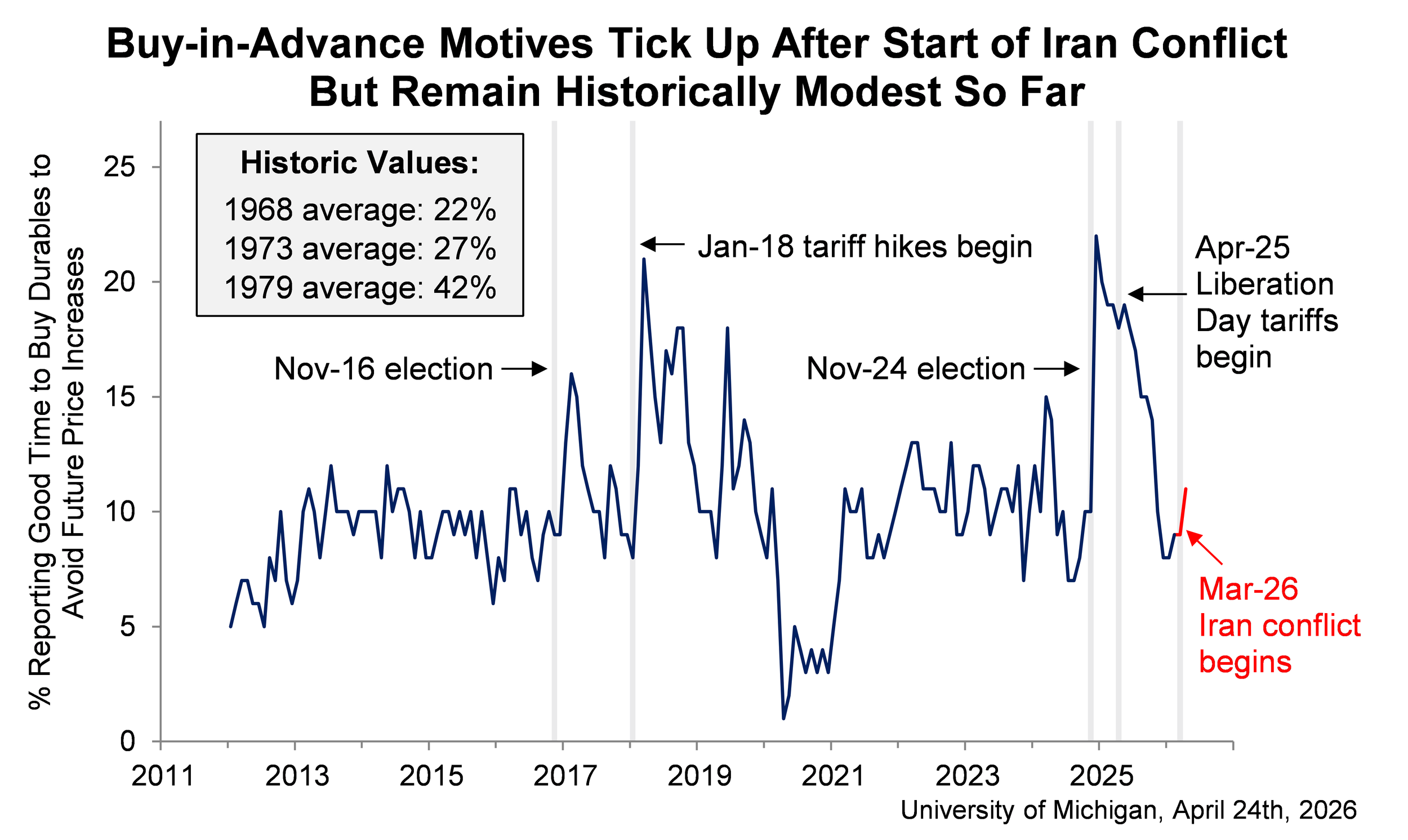

The University of Michigan’s final April Consumer Sentiment Index came in at 49.8. That number is the lowest reading on records going back to 1952 — lower than the 2008 financial crisis, lower than the 2022 inflation peak, lower than COVID. Sentiment dropped 3.5 points from March, with declines spanning every demographic group, income bracket, and political affiliation, according to the University of Michigan Surveys of Consumers (April 24, 2026).

The data point that matters most for retail tenants and the consumers who shop with them: one-year inflation expectations jumped from 3.8% in March to 4.7% — the largest one-month jump since April 2025, CNN Business reported on April 24. When consumers expect prices to keep rising, they trade down, eat at home more, and delay big-ticket purchases. That re-anchoring of inflation psychology is happening in real time, and it directly affects the foot traffic and ticket sizes at the tenants who occupy your inline space.

The energy picture is no longer best understood as a “spike.” It’s the new baseline households are operating in. AAA’s national average for regular gasoline is at $4.05 a gallon as of April 24, per AAA Newsroom. WTI is back near $93. Brent crude topped $106 yesterday as Strait of Hormuz tensions re-escalated, Al Jazeera reported. The Iran war is now in its eighth week.

There is also a significant optical illusion in the March retail sales report. Headline retail sales jumped 1.7% — the biggest monthly increase since January 2023, per the U.S. Census Bureau (April 21, 2026). On its face, that suggests a consumer boom. But the Census report is not adjusted for price changes, and gasoline station receipts surged a record 15.5% for the month. Strip out the gasoline distortion and the consumer is materially weaker than the headline suggests. Consumers aren’t buying more — they’re paying more for the same gallon.

The labor market remains one bright spot. Initial jobless claims came in at 214,000 for the week ending April 18, per the U.S. Department of Labor (April 23, 2026). That’s still inside the historically healthy 200K–250K range we’ve been in since the post-pandemic recovery. Hiring has tapered, but firings haven’t accelerated.

On the rates side, the 10-year Treasury closed April 23 at 4.30%, per the Federal Reserve H.15 release. Shopping center loan rates are starting around 6.32% as of April 15, per Select Commercial — a function of the war’s inflation premium being priced into the long end of the curve.

If that’s all the data you saw, you would assume strip center fundamentals were under serious pressure. Here’s the problem with that conclusion: the actual leasing data this week says the opposite.

The Strip Center Disconnect

On April 23, Phillips Edison & Company reported its Q1 2026 results. For readers who don’t follow public REITs, PECO owns about 290 grocery-anchored neighborhood centers across 31 states, totaling roughly 30 million square feet. They are the cleanest public-market read on the kind of asset most strip center owners actually own — not a mall REIT, not a power center REIT, not a net lease REIT, but a portfolio of the everyday neighborhood centers that define our market.

The Q1 2026 numbers, from the PECO earnings release:

Leased portfolio occupancy: 97.1%

Inline occupancy: 95.0%

Comparable renewal rent spreads: 21.2%

Comparable new lease rent spreads: 36.2%

Comparable inline new lease rent spreads: a record-high 37.9%

Same-center NOI growth: +3.5% year-over-year

Average annual rent bumps on inline leases: 2.7%

While consumer sentiment was hitting an all-time low, neighborhood center landlords were re-leasing inline space at 37.9% above the prior tenant’s rent. That is structural rent growth occurring in the same week the macro headlines were screaming stagflation.

A necessary caveat: PECO is grocery-anchored. Most strip center owners — particularly in our San Antonio, Austin, and Rio Grande Valley markets — own unanchored or shadow-anchored centers. The grocery anchor base gives PECO a slightly different tenant mix and credit profile than a pure unanchored Texas strip. You should not expect to replicate identical 36% new lease spreads when you re-tenant your inline suite.

But the directional read is real, and it’s the most useful single data point a strip center owner could have this week. On-the-ground demand for well-located neighborhood retail space is stronger right now than it has been in years. There are three structural reasons this is true, and they compound each other.

No new supply. Strip mall construction has been essentially frozen for the past two-plus years. High construction costs, elevated borrowing costs, and the long lead times on entitlements have all worked together to keep new product from coming online. The neighborhood centers you own today are irreplaceable at current rents — a new build would have to clear a much higher rent threshold to pencil.

Vacancy is near historic lows. National retail vacancy is sitting around 4–5%, and unanchored strip centers are running about 4.5% vacancy nationally, according to Matthews Real Estate Investment Services (H2 2025). When tenants need space, they’re competing for what already exists.

The closure pipeline is concentrated in the wrong places — for you. Coresight Research projects U.S. retailers will close about 7,900 stores in 2026, down 4.5% from 2025, while opening about 5,500, per CNBC’s coverage of the Coresight forecast. The closures are concentrated in legacy mall-based names — Eddie Bauer, GameStop, Saks Off 5th, Walgreens — not in the inline neighborhood center space your tenants occupy. The vacated space is creating new opportunities, not new pressure.

Tenants on the Right Side of the Bifurcation

If you have a vacant suite, a renewal coming up, or you’re underwriting a potential acquisition, here are the tenant categories your broker should be hunting for.

Fitness and wellness. Crunch Fitness alone is targeting more than 100 new openings in 2026. Levin Management reports that 40% of their portfolio centers now have a fitness tenant, totaling nearly 330,000 square feet, per Chain Store Age (March 9, 2026). Boutique concepts including Stretch Zone, HOTWORX, and pickleball facilities are all chasing space. The fits range from 1,500 SF for a stretch concept up to 30,000+ for a full-service gym, and second-generation pharmacy boxes are particularly attractive given their typical 12,000–14,000 SF footprint.

Medtail. Urgent care, dental, vision, and specialty wellness now account for about 20% of leased medical space in retail buildings, up from roughly 16% in 2010, per Cushman & Wakefield’s medtail report. Tenant improvement investments for a medtail buildout often run $200 to $300 per square foot — sometimes higher — which makes these the stickiest leases on your rent roll. The infrastructure investment is so substantial that medtail tenants rarely move once installed. Endcaps and outparcels with strong visibility and easy parking are ideal, but watch your parking ratios — urgent care typically requires 5–6 spaces per 1,000 SF versus 3 for general retail.

Quick-service restaurants with drive-thrus. Beverage concepts including 7 Brew, Dutch Bros, and Swig continue aggressive expansion in Texas. Chicken concepts and coffee continue to lead unit growth nationally. Pad sites and outparcels remain red-hot in our markets. One caution flag: long-term, ground lease rents on drive-thru sites are getting tested by underwriters who want to confirm tenant volumes can support the rent. Don’t let one strong recent comp anchor your pricing for every pad in your trade area.

Service tenants — the inline backbone. Look at recent strip center transactions in Texas — Princeton Plaza near Dallas (Tropical Smoothie, Pizza Hut, HOTWORX, Modern Nail Bar, Princeton Dental) and Cross Creek Plaza in Fulshear (Five Guys, Cold Stone Creamery, Floreo Nail Spa) — and you see the same tenant mix repeating. Smoothies, ice cream, nail salons, dental, fitness, vape shops. Local-services oriented. Internet-resistant. Time-saving for the consumer. That is the entire pitch of an unanchored neighborhood center, and it’s working.

CRE Takeaway: Three Things Strip Center Owners Should Do This Week

First, mark-to-market your inline rent roll. If PECO is reporting record-high 37.9% rent spreads on comparable inline new leases, your in-place rents are very likely below market — particularly if your last leasing cycle predates 2023. The action: pull every lease expiring in the next 24 months. Build a market rent comp book for your trade area, drawing on your broker, your peers, and recent strip center sales like the Texas comps mentioned above. Do not sign a renewal at last cycle’s rates without first understanding what a brand-new tenant would pay for the same space. The macro tape is fragile, but your asset’s leasing market is structurally strong. Don’t let the headlines talk you into accepting less than what your space is worth.

Second, treat anchor turnover as a rent reset opportunity, not a credit event. Simon Property Group reported on its Q4 2025 earnings call that 38 Saks Off 5th leases that were rejected in bankruptcy were re-tenanted at a +67% rent spread, meaning the new tenants are paying 67% more than the old anchor was paying, per analysis from mmcginvest’s Great American Store Closure Tracker (April 19, 2026). If you have a struggling anchor or a junior anchor coming up on renewal, do not panic — model the mark-to-market upside before you make any decisions. The tenant pipeline behind a backfill is deeper than it has been in a decade. A vacated 12,000 SF box might be worth more in year one of a new lease than it was in year ten of the old one. This is a different mental model than the one most owners have been operating with for the past five years.

Third, run hold-vs-sell math on your actual asset, not on 2024 assumptions. Borrowing rates are elevated — strip center loans are starting around 6.32% with the 10-year at 4.30%. That’s real, and it pressures cap rates. But your forward NOI growth is materially better than what underwriters were modeling 18 months ago. PECO’s same-center NOI grew 3.5% year-over-year in Q1 2026, and inline leasing deals are getting average annual rent bumps of 2.7%. Don’t anchor your hold/sell decision on 2024 cap rate spreads. If you have inline leases rolling, your forward NOI growth could justify holding — or it could create the cleanest sale moment you’ve had in years if a buyer is willing to underwrite the rent reset upside. There is no one-size answer, and the math on your specific asset is the only thing that matters.

The Bottom Line

The macro picture is genuinely difficult. Sentiment at an all-time low is not a number you wave away, and the inflation expectations re-anchoring is going to flow through to your tenants’ top lines in the coming quarters.

But the leasing market for well-located neighborhood retail real estate is, on the data, having one of its strongest moments in years. There is a real, measurable disconnect between the macro headlines and what is actually happening in the rent rolls of the assets we sell and advise on. Both things are true at the same time. Both are showing up in the data this week.

Don’t let one set of data convince you to ignore the other.

If you’re thinking through your hold period, your refi timing, your tenant mix, or your exit strategy, this is the kind of week where the right 30-minute conversation can save you a six- or seven-figure mistake. That’s the work we do every day with strip center owners across San Antonio, Austin, and the Rio Grande Valley.

Reach out anytime.

Ray Kang, CCIM

Commercial Real Estate Investment Sales Advisor

Strip Centers — San Antonio | Austin | Rio Grande Valley

StripCenterIQ.com | raycrebroker.com

🎙️ [WATCH OR LISTEN ON YOUTUBE ▶️]

This article is for informational purposes only and does not constitute investment, legal, or tax advice. All data and forecasts are subject to revision. Always consult qualified professionals before making investment decisions.