The Rate Cut That Isn’t Coming — And What It Means for Strip Center Owners in 2026

For two years and four months, the entire commercial real estate industry has been waiting on the same thing: a rate cut big enough to actually move cap rates.

This week, the Fed didn’t cut. That’s not the news.

The news is that three regional Fed presidents broke ranks Wednesday and tried to remove the language that says rate cuts are even on the table — while oil punched back through $100 a barrel, Q1 inflation re-accelerated to 4.5%, and the consumer side of GDP decelerated to 1.6% growth.

If you own a strip center in San Antonio, Austin, or the Rio Grande Valley, this changes the math on your hold-versus-sell decision. Not next year. Right now.

This week’s edition of the Retail Weekend Wrap-Up walks through what happened, what it means for borrowing costs, and — most importantly — how it should change how you think about your tenant mix for the next twelve to eighteen months.

Story 1: The Fed Just Tried to Take the Rate Cut Off the Table

On Wednesday, April 29, the Federal Open Market Committee held the federal funds rate steady at 3.50% to 3.75%. Markets had priced in a 100% probability of a hold heading into the meeting. That part was a non-event.

What wasn’t a non-event: the vote was 8-4. Four dissents — the most at a single FOMC meeting since October 1992, a 34-year stretch.

The composition of those dissents matters far more than the count. Governor Stephen Miran was the only dissenter who wanted a quarter-point cut, and he has been pushing for cuts at the past six consecutive meetings. That’s a familiar dissent. Markets discount it.

The other three are the ones to pay attention to.

Cleveland Fed President Beth Hammack, Minneapolis Fed President Neel Kashkari, and Dallas Fed President Lorie Logan all voted against the policy statement — not because they wanted a different rate today, but because they wanted the easing bias removed from the statement language entirely. They wanted the forward guidance to read as neutral. As in: a hike is now just as likely as a cut.

In his post-meeting press conference, Powell himself acknowledged that more committee members wanted the statement to communicate, in his words, a neutral stance. He framed it within a broader supply-shock context — naming the pandemic, the invasion of Ukraine, the tariffs, and now Iran and the oil spike as four major shocks that have made the path of policy unusually difficult.

This was Powell’s last meeting as Fed Chair. His term expires May 15. Kevin Warsh’s nomination cleared the Senate Banking Committee the same day, advancing to the full Senate for confirmation. The dissents from Hammack, Kashkari, and Logan have been widely interpreted in the financial press as a signal to the incoming chair that the regional presidents will not rubber-stamp a dovish pivot.

What This Means for Strip Center

The 10-year Treasury closed Thursday at 4.40% — up from where it traded heading into the meeting, and a clear signal that the bond market interpreted the dissents as hawkish.

Walk through the math on a refinance or acquisition today:

10-year Treasury (lender base): 4.40%

Lender spread on a strip center loan: 250 to 275 basis points (typical range for stabilized retail in our markets)

Resulting loan rate: 6.90% to 7.15%

Now consider the deal math. On a strip center acquired at a 7.50% cap rate with 65% LTV financing at 7.00%:

Year-one debt service consumes roughly 78–82% of NOI, depending on amortization

Debt coverage ratio (DCR) lands in the 1.20–1.25 range

Cash-on-cash return to the equity sits in the 7.0–7.5% range

If you’ve been modeling a refinance in late 2026 with a 5.25% to 5.50% loan rate, that scenario just got materially less likely. The owners I’m talking to who were waiting out the rate cycle — this is the week to re-run your numbers honestly.

A deal that pencils at a 1.30 DCR and a 7.25% cash-on-cash today is a real deal. A deal that requires a rate cut to pencil is a hope, not a deal.

Sources: Federal Reserve FOMC Statement, April 29, 2026; CNN Business, April 29, 2026; Federal Reserve H.15 Selected Interest Rates

Real GDP, Percent Change From Preceding Quarter (Q4 2024 – Q1 2026). Source: U.S. Bureau of Economic Analysis.

Story 2: Q1 GDP — A 2.0% Print That’s Weaker Than It Looks

Thursday morning, the Bureau of Economic Analysis released the advance estimate for Q1 2026 GDP. The headline number: real GDP grew at a 2.0% annualized rate, up from 0.5% in Q4 2025.

On the surface, that looks like a clean rebound. Read the composition and it’s a different story.

Three things did most of the lifting: Federal employee compensation snapped back after the late-2025 government shutdown, AI-related business investment surged roughly 10%, and government spending rose 4.4% overall with federal spending up over 9%.

Personal consumption decelerated to 1.6% growth. The engine of the U.S. economy — accounting for roughly two-thirds of GDP — grew slower than the headline number suggests.

The PCE price index inside the same release came in at 4.5% for the quarter, up sharply from 2.9% the prior quarter. Core PCE — the Fed’s preferred inflation gauge — rose to 4.3% from 2.7%. That is the number that gave the regional Fed presidents the cover to push for removing the easing bias.

What This Means for Strip Center

Strip center NOI is built on tenant sales, and tenant sales are built on consumer spending — not on AI capex and not on federal back pay. When the consumer line decelerates while the headline accelerates, what you’re seeing is a high-tide GDP print covering a falling-tide consumer.

If you own a center anchored by discretionary categories — apparel, casual dining, full-service restaurants, specialty retail — pull your tenant sales reports for Q1 and look year-over-year. Tenants who are flat-to-down on a 1.6% consumer-growth quarter become tenants who are negative when growth slows further.

Vacancy risk shows up six to nine months before the lease expires. Underwriters and buyers will price that risk aggressively in 2026 acquisitions.

Source: BEA GDP Advance Estimate, 1st Quarter 2026, released April 30, 2026

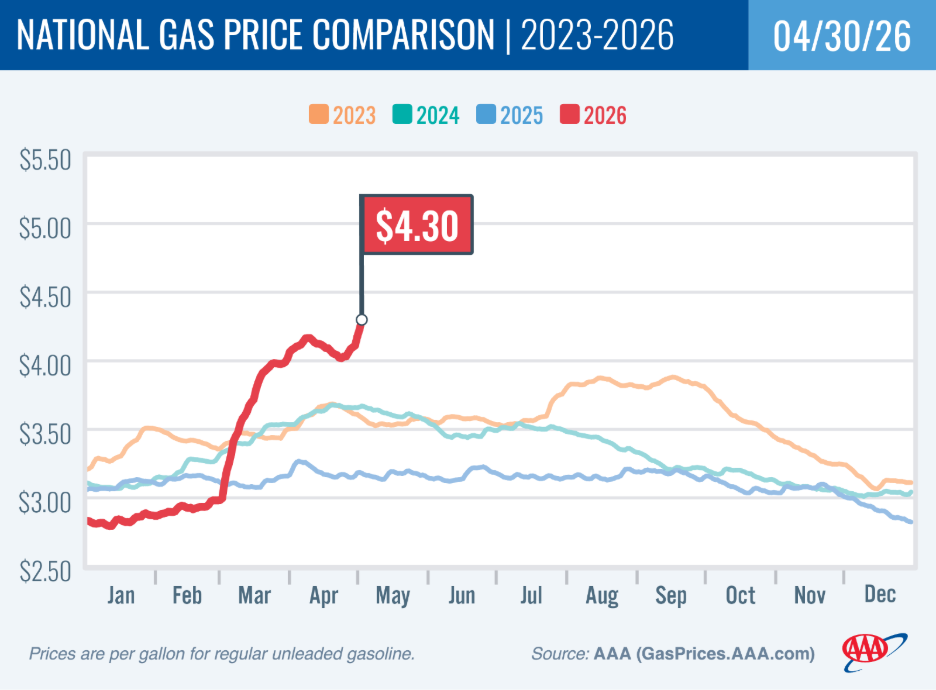

Story 3: Oil Above $100 Again, Gas at Four-Year Highs

AAA’s update Wednesday: the national average for regular gasoline jumped 27 cents in a single week to roughly $4.27 per gallon — $1.12 per gallon higher than this time last year, and the highest national average since late July 2022.

What drove the jump: WTI crude settled at $106.88 a barrel Wednesday after a $6.95 single-day move. Brent traded above $111 Friday morning. The Strait of Hormuz remains effectively closed, the U.S.-Iran peace talks hit an impasse this week, and the Trump administration is enforcing a blockade on Iranian ports.

If there’s any silver lining for our markets, Texas is currently the ninth-cheapest state at the pump at roughly $3.85 per gallon — about 42 cents below the national average. But $3.85 is still well above where Texas drivers were paying twelve months ago, and the relative discount doesn’t insulate the consumer.

What This Means for Strip Center Owners

Every dollar above the long-run average gas price is a dollar pulled out of discretionary retail spending in your trade area. The consumer doesn’t have the option to drive less — they have to get to work, school, doctor’s appointments. The pump price is functionally a tax on everything else in the household budget.

That’s bad for the apparel tenant, the casual-dining tenant, and the discretionary-services tenant in your center. It is not bad for grocery, dollar-store, beauty/personal care, urgent care, fitness, and value-oriented tenants. Sustained $4-plus gas accelerates the consumer trade-down that has been building for two years.

If you’re underwriting a center for sale in 2026, this is the dynamic the buyer is going to model. The broker who walks in with a credible read on tenant durability under sustained $4-plus gas is the one who is going to defend the price.

Source: AAA Gas Prices, April 30, 2026

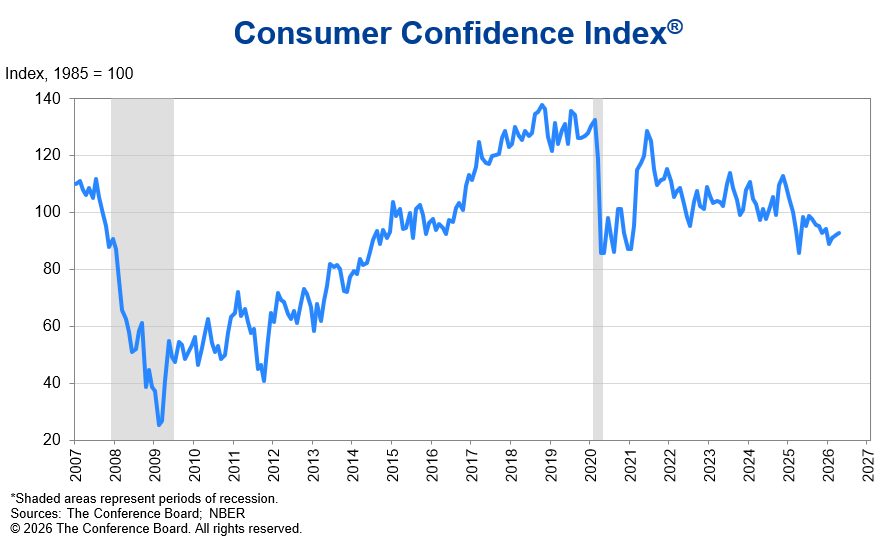

Story 4: Consumer Confidence — The Headline vs. the Subtext

The Conference Board released April consumer confidence Tuesday. The headline number ticked up 0.6 points to 92.8 — the third straight monthly increase, and well above the 89 that economists had expected. On paper, that reads like a resilience story.

Look one layer down and there’s a clear split: The Present Situation Index (how consumers feel about right now) fell 0.3 points to 123.8, while the Expectations Index (how they feel about the next six months) rose 1.2 points to 72.2. The whole gain came from forward optimism. The survey period — April 1 through April 22 — coincided with the temporary two-week ceasefire that started April 8 and the equity rebound that followed. That ceasefire has since collapsed, and oil is back above $100.

Consumers planning more spending on services over the next six months shifted from “yes” and “maybe” to “no” in April. Anticipated future spending fell across nearly every services category — restaurants, hotels, airfare, beauty. The one category that rose: pet care.

Conference Board’s chief economist Dana Peterson noted that mentions of prices, oil and gas, and war all increased in the open-ended responses compared to March.

What This Means for Strip Center Owners

The mix shift inside services spending is what matters for strip center underwriting. “Cheap thrills and necessary services” is how the Conference Board characterized the pattern.

Holding up: Nail salons and beauty under $50/visit, urgent care, pet care and pet supply, fast-casual restaurants under $15/check, discount and value retailers, personal care services.

Actively softening: Sit-down dining and full-service restaurants, salons doing $200+ services, specialty fitness at $200/month, specialty apparel, travel-adjacent retail.

If your center is heavily weighted to the second list, the question to ask yourself in May 2026 isn’t whether tenants are paying rent today. They are. The question is what their renewal looks like in 2027 and 2028 if this consumer pattern holds for another four quarters.

Source: The Conference Board Consumer Confidence Index, April 28, 2026

Story 5: 9,500 Independent Restaurants Closed in 2025. Chains Added 3,600.

This is the story to remember if you remember nothing else from this week.

On Tuesday, Restaurant Business published Technomic’s full-year 2025 unit-count data: Independent restaurants in the U.S. declined 2.3% in 2025 — a net loss of approximately 9,500 locations in twelve months. The top 500 restaurant chains grew their unit count 1.5% over the same twelve months — adding roughly 3,600 net new units. Chains now represent about 35% of the entire restaurant industry, a record share.

Technomic’s senior principal David Henkes laid out the cause plainly: every input cost — labor, rent, insurance, food — has risen at mid- to high-single-digit rates. Chains have deeper pockets, better procurement leverage, and more capital to weather a 5–10% traffic decline. Independents do not. Black Box Intelligence projects 9% of full-service restaurants and 4% of limited-service restaurants are at risk of closure in 2026.

What This Means for Strip Center Owners — Two Strategic Moves

First: Re-sign your durable independents early. If you have an independent restaurant tenant who is current on rent and has been operating five-plus years through this cycle, that tenant is more valuable than a market-rate replacement chain. A modest concession — a small rent reduction, a one-year extension at flat terms, or a percentage-rent provision — to secure a 5-to-7-year extension with a proven operator is almost always cheaper than carrying the alternative.

Second: If you’re carrying a vacant restaurant box, the chains have leverage right now. The deals you sign in 2026 will look different from the deals you signed in 2022. Chains are being selective. Expect more aggressive rent concessions and TI requests, longer free-rent periods, more demanding co-tenancy clauses, and more resistance to standard percentage-rent escalations.

If you’re thinking about selling: A center anchored by surviving independents and growing chains tells a very different story to a buyer than a center with two dark restaurant boxes. Tenant durability is the underwriting variable that gets the price defended.

When I take a property to market in the current environment, the credible answer to “what does this rent roll look like in 2027?” is what closes the gap between what the seller wants and what the buyer is willing to pay. The data this week makes that question more important — not less.

Source: Restaurant Business, citing Technomic, April 29, 2026

Here’s what this week is really telling you.

The market spent two years assuming the Fed would eventually rescue commercial real estate values through a meaningful rate cut. This week, three regional Fed presidents publicly signaled they don’t think that cut is coming. Oil is back above $100. Inflation is reaccelerating. The consumer is decelerating. And the tenant base under your strip center is sorting itself into winners and losers in real time.

None of that is a reason to panic. All of it is a reason to stop waiting.

The hold-versus-sell decision in 2026 is not the same decision it was in 2024. It is a different cost-of-capital environment, a different tenant environment, and a different buyer pool. The right answer depends entirely on your specific property, your specific basis, your specific debt maturity, and your specific tenant mix.

Watch on Youtube

If you own a strip center in San Antonio, Austin, or the Rio Grande Valley and you want a real, no-pitch read on what your property would do in today’s market — what cap rate it commands, what your buyer pool looks like, and what tenant moves would defend value before you go to market — that’s the conversation I want to have with you this month.

Reach out through my scheduling page or message me directly on LinkedIn. I read every inquiry personally.

See you next Saturday.

— Ray Kang, CCIM

StripCenterIQ | raycrebroker.com

The Bottom Line for Strip Center Owners