Hired But Hesitant: What the May 8 Data Drop Means for Strip Center Owners

By Ray Kang, CCIM | StripCenterIQ | May 8, 2026

Two significant data releases arrived simultaneously this morning, and they are telling conflicting stories about the American consumer. Understanding the tension between them is the most important thing a strip center owner can do with the next ten minutes.

The Jobs Number: Stronger Than Expected

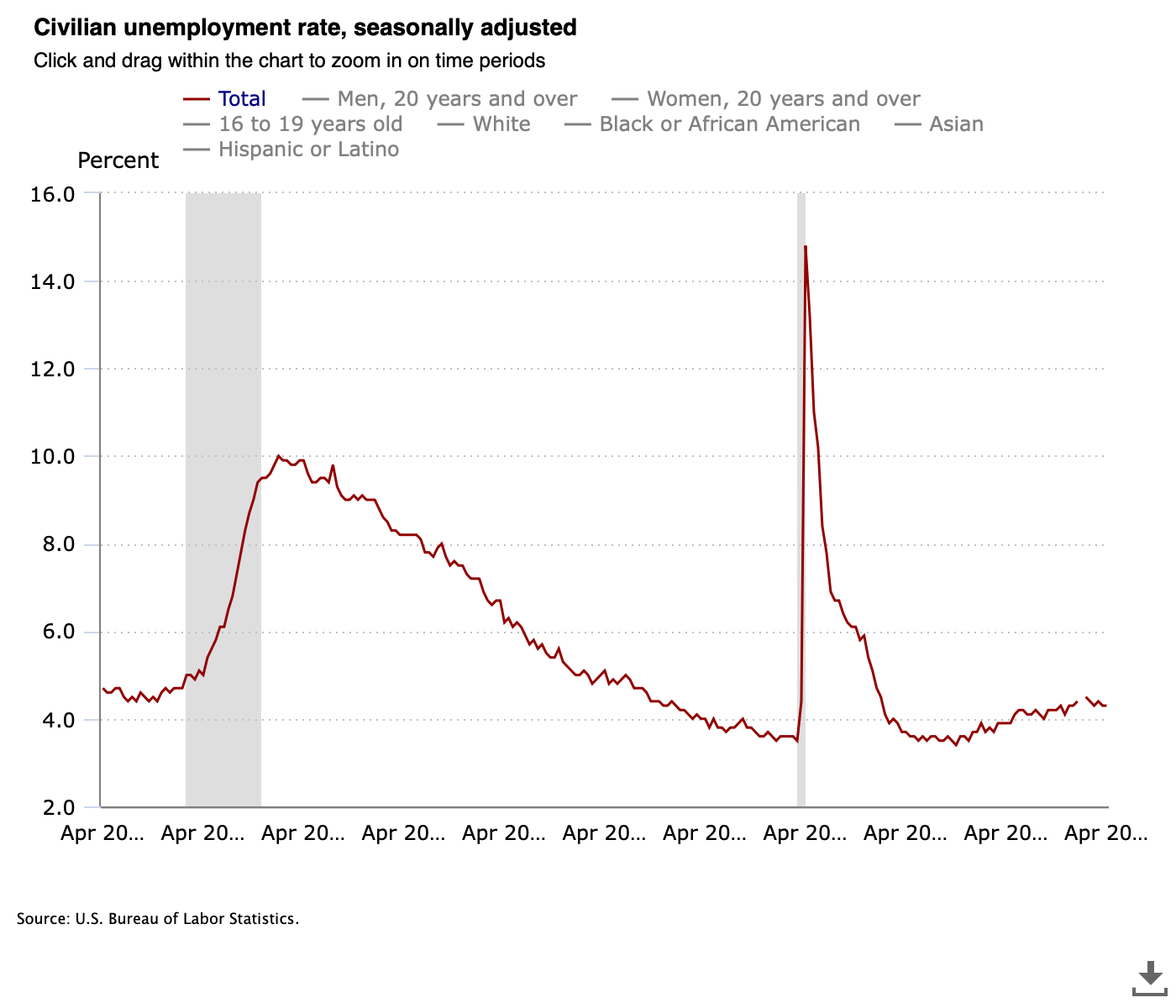

The U.S. Bureau of Labor Statistics released the April 2026 Employment Situation this morning. The economy added 115,000 jobs last month against a consensus forecast of 62,000 — nearly double what economists were expecting. Retail trade added 22,000 positions specifically. The unemployment rate held steady at 4.3%.

For context: February was revised down to -156,000 jobs — a contraction. March came in at +185,000. April's +115,000 represents the first back-to-back monthly gains in nearly a year. The labor market is not broken. It is cooling, but it is not in freefall.

For strip center owners, this matters because employed consumers drive foot traffic. A resilient labor market keeps the base of your tenants' customer pool intact. People who are working spend money. Not always freely — but they spend.

The Sentiment Number: A Four-Year Low

On the same morning, the University of Michigan Surveys of Consumers released preliminary May 2026 data. Consumer sentiment dropped 3.5 points, landing at a level the researchers described as "comparable to the trough seen in June 2022." That was not a good period for discretionary retail.

The more striking figure: year-ahead inflation expectations surged from 3.8% to 4.7% in a single month. That is the largest one-month jump in inflation expectations since April 2025. The Michigan survey specifically noted that declines in sentiment were seen "across political party, income, age, and education." This is not a partisan or demographic artifact. It is broad.

What drives this? The report points directly to the ongoing Iran conflict and its effects on gasoline prices. "The Iran conflict appears to influence consumer views primarily through shocks to gasoline and potentially other prices," the researchers noted.

Gas at $4.55 — The Pump Gets Paid First

The AAA national average for a gallon of regular gasoline was $4.55 on May 7, 2026 — up 25 cents for the second consecutive week, and $1.40 higher than the same week a year ago. This is the highest average of 2026 so far. The primary driver is the Strait of Hormuz conflict, which has disrupted global oil supply and triggered significant volatility in energy markets.

This matters for your strip center in a specific way: every dollar a household spends at the pump is a dollar that does not reach your tenants. The Census Bureau's March retail sales report showed a 1.7% headline gain — but that was largely driven by a record 15.5% surge in gasoline station receipts. Inflation-adjusted retail sales are up only 0.7% over the past twelve months and remain below their April 2022 peak. The headline number flatters the underlying consumer.

There is a potential relief valve: reports as of this week indicate that the United States and Iran are close to a framework agreement that could reopen the Strait of Hormuz. If confirmed, oil prices and gas prices would be expected to fall relatively quickly. The 10-year Treasury yield, which briefly spiked to 4.41% mid-week as energy fears peaked, has already pulled back to 4.38% on these reports. Watch oil markets closely over the next two weeks. This is a live variable in your tenants' operating environment.

Where the Consumer Is Actually Spending

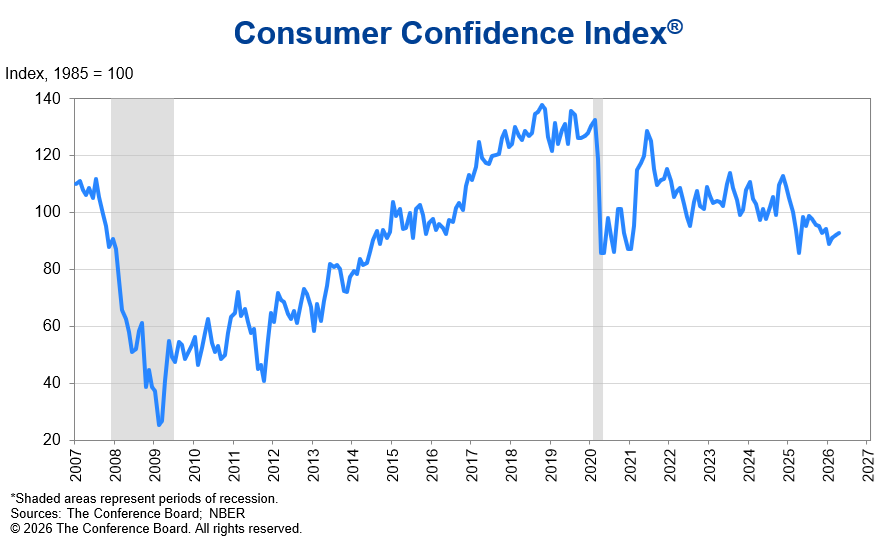

The Conference Board's April 2026 Consumer Confidence report provides the clearest picture of where consumer dollars are actually going. The Board's language is precise: spending in 2026 is concentrating in "cheap thrills and necessary services."

The top expected spending category for the next six months: restaurants, bars, and takeout — ranked first. Beauty and personal care followed, along with streaming/mobile services and health and personal care. Meanwhile, spending intentions for travel, big-ticket purchases, and expensive discretionary services are declining.

This data provides a direct tenant-mix signal for strip center owners. The concepts doing best with this consumer profile:

Quick service and fast casual restaurants (especially value-positioned; Restaurant Dive's 2026 outlook notes QSR is gaining market share as consumers trade down from pricier fast casual options)

Neighborhood dining and takeout-forward concepts

Beauty and personal care services (nail salons, hair salons, medspas)

Health and wellness (urgent care, dental, optometry, fitness)

Value retail (dollar stores, discount grocery, off-price)

The concepts facing a more difficult environment: mid-tier apparel, home goods, entertainment-focused tenants, and anything requiring consumers to feel optimistic about discretionary spending.

The Fed: A Leadership Transition Into a Frozen Environment

On April 29th, the Federal Reserve held the federal funds rate target range at 3.5%–3.75% for the third consecutive meeting. The vote was 8-4 — the most divided Federal Reserve decision since October 1992. One dissenting member voted to cut immediately. Three others voted against language in the statement that even implied future cuts were on the table.

This is a committee without consensus on the direction of rates. It is also a committee about to change leadership.

On May 15th, Kevin Warsh assumes the role of Federal Reserve Chair, replacing Jerome Powell. Warsh inherits a divided committee, a 10-year Treasury at 4.38%, and a consumer inflation expectations reading that just jumped to 4.7% — the highest level in over a year.

Markets are currently pricing approximately a 20% probability of a rate cut before September or October 2026. The higher-for-longer rate story is not over. It has a new author.

What this means for deal math: When you combine a 10-year Treasury at 4.38% with a typical commercial lender spread of 200 to 250 basis points, you get commercial mortgage rates in the 6.4% to 6.9% range on most strip center transactions. At those rates:

Debt coverage ratios require higher NOI to satisfy lender thresholds

Cash-on-cash returns compress unless purchase prices adjust downward

The buyer pool narrows to those who can either bridge the gap with equity or underwrite to future rate relief

If you are planning a disposition or acquisition in 2026, model your timeline around a rate environment that is not meaningfully different from today. The new chair does not have a mandate to cut quickly — and inflation expectations of 4.7% give the committee political cover to hold.

The Tenant Landscape: Who's Growing, Who's Shrinking

Coresight Research projects approximately 7,900 store closures nationally in 2026, representing a 4.5% decrease from 2025's total. The active closure names most relevant to strip center owners include Francesca's (all approximately 400 locations in liquidation), Saks OFF 5TH (57 closures in Chapter 11 restructuring), Kroger (approximately 60 underperforming stores over 18 months), and Walgreens (continuing a multi-year plan to reduce its footprint by 1,200 locations over three years).

On the expansion side: Dollar General, Aldi, and Tractor Supply lead new store opening plans. This is the tenant mix rotation in real time — value-oriented, essential, needs-based retail expanding into the gap left by mid-tier and department-store-adjacent concepts.

New strip center construction remains constrained. High labor costs and elevated borrowing rates have kept development starts low, which means well-located existing strip center space is genuinely scarce. As one industry analyst noted, this creates a "dwindling supply" dynamic that may become a significant constraint by 2029 and 2030.

For owners with upcoming lease expirations: the supply constraint works in your favor when negotiating with expanding value tenants. For owners with a Walgreens or similar pharmacy anchor in an option window: understand your re-leasing exposure before that conversation arrives.

What This Means for Your Property

The question this week is not whether the economy is good or bad. It is more specific: does your tenant mix map to where the consumer is actually spending?

If your strip center carries QSR anchors, neighborhood restaurants, beauty services, health and wellness, and value retail — you are sitting in the strongest demand pocket of this market cycle. Those tenants are growing, their customers are coming, and their lease renewals are supportable.

If your center carries mid-tier apparel, home goods, or concepts that depend on consumer optimism — you are managing into a headwind. That doesn't mean you are in trouble. It means the next lease negotiation is more work, and the next buyer conversation requires a more detailed narrative about the path forward.

The labor market is holding. The consumer is cautious. The rate environment is frozen. The tenant rotation is accelerating. Those four facts, taken together, define the strip center owner's challenge for the next twelve months — and they define the opportunity for anyone positioned correctly.

If you own a strip center in San Antonio, Austin, or the Rio Grande Valley and want to talk through what this market picture means for your specific property, reach out. This is exactly the kind of conversation I have with clients every week.

WATCH OR LISTEN ON YOUTUBE ▶️

Ray Kang, CCIM is a commercial real estate investment sales advisor specializing in retail strip centers across San Antonio, Austin, and the Rio Grande Valley, Texas. StripCenterIQ is his weekly market intelligence series for strip center owners and investors.